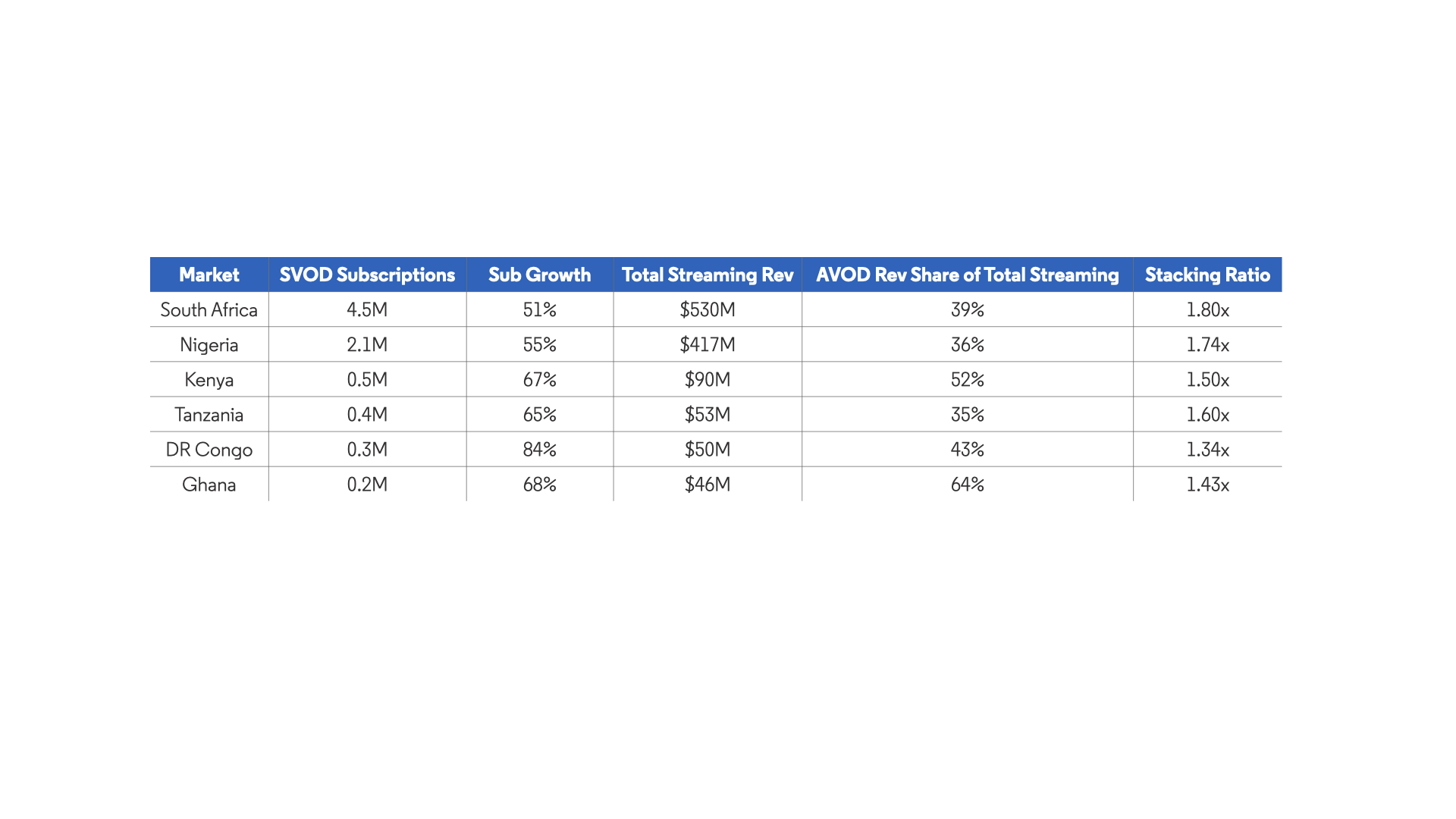

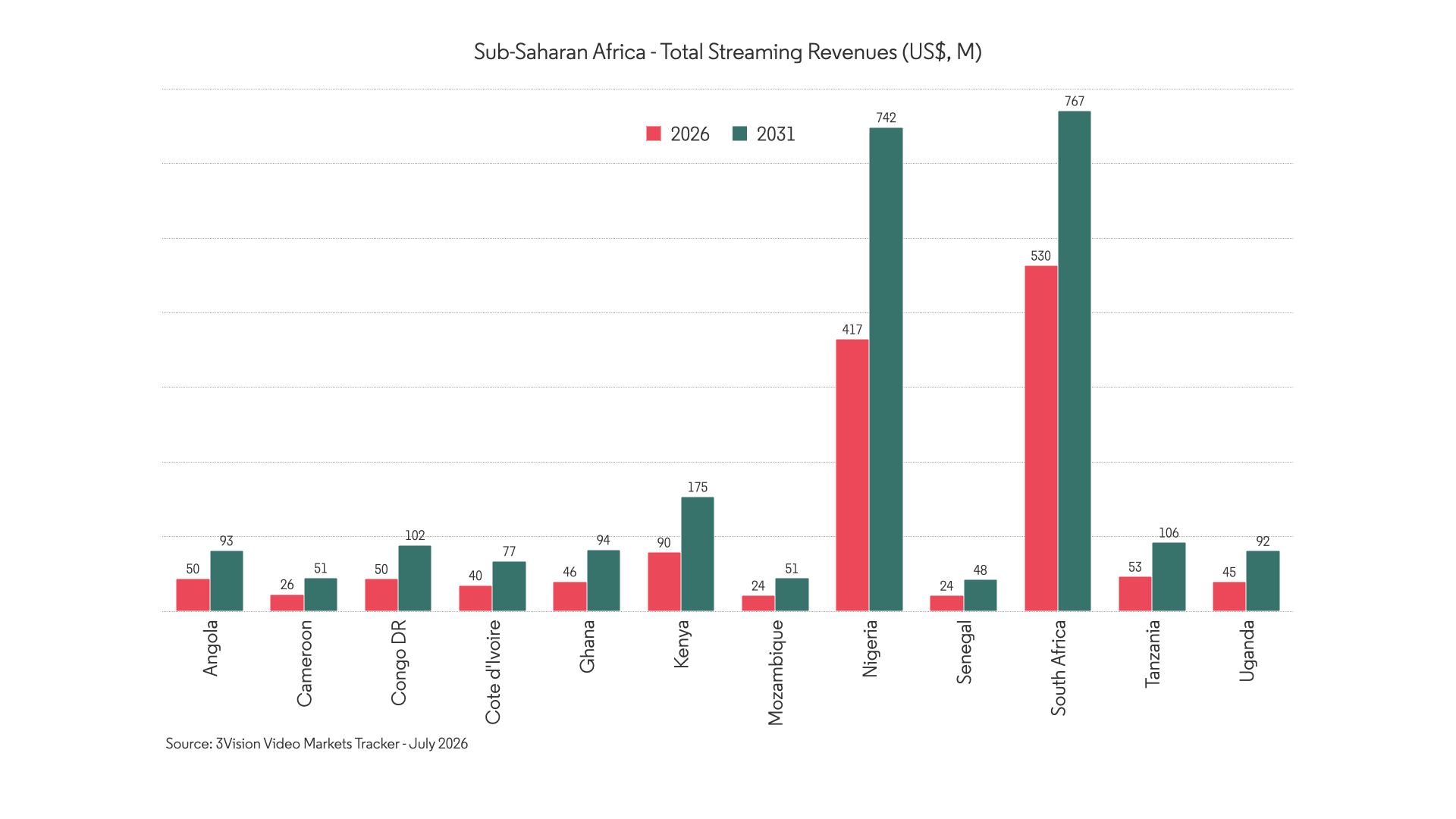

South Africa: 4.5M SVOD subscriptions in 2026, rising to 6.8M by 2031 (+51%) | Total streaming revenues $530M, reaching $767M (+45%)

Nigeria: 2.1M SVOD subscriptions in 2026, rising to 3.2M by 2031 (+55%) | Total streaming revenues $417M, reaching $742M (+78%)

East Africa: 1.2M SVOD subscriptions in 2026, rising to 2.1M by 2031 (+75%) | Total streaming revenues $189M, reaching $374M (+98%)

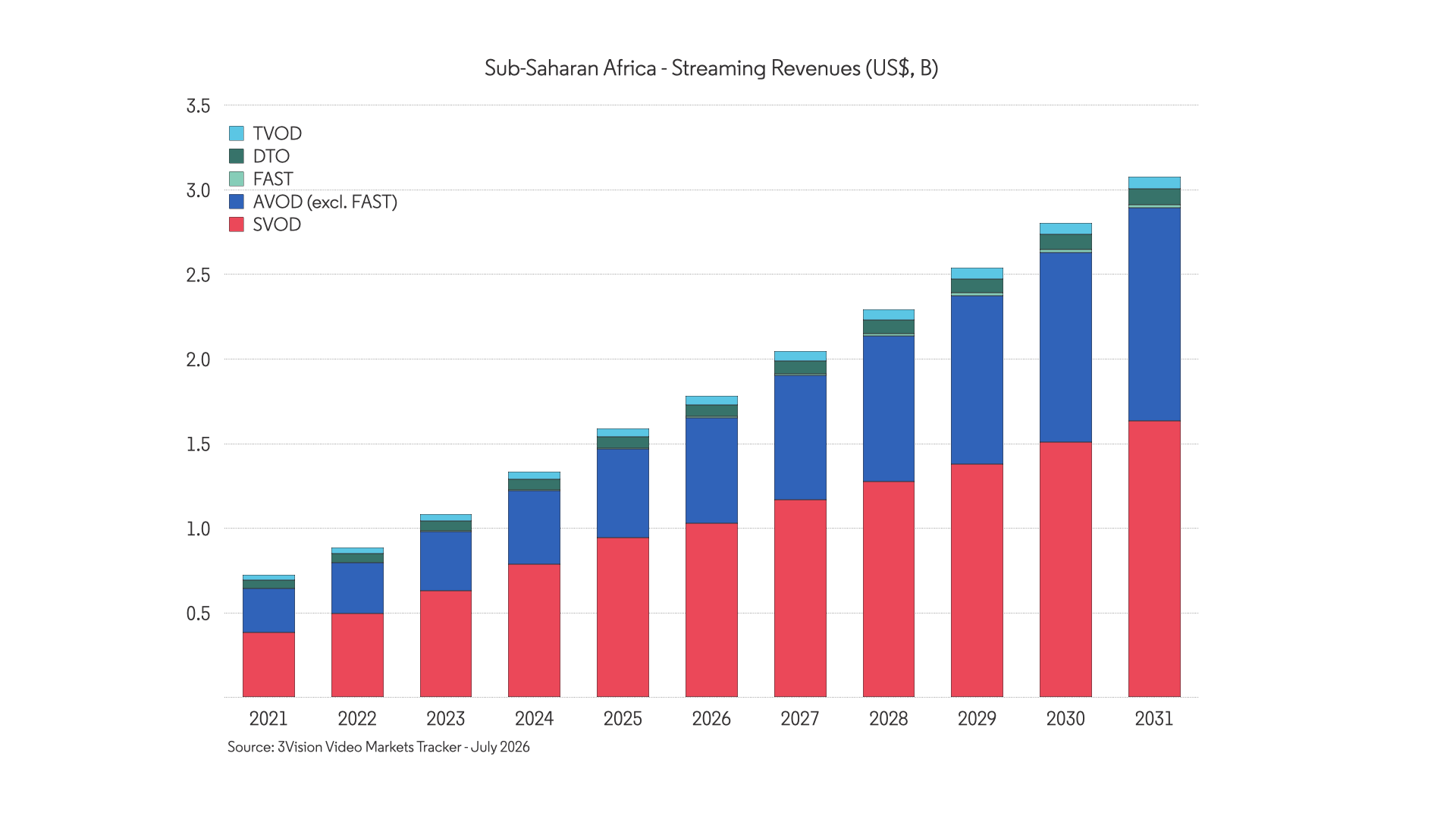

Regional Total: 11.0M SVOD subscriptions | $1.8B in total streaming revenues in 2026, reaching $3.1B by 2031

Key Findings:

- Sub-Saharan Africa is the world's fastest-growing streaming region by revenue, and it is being built on advertising as much as subscription. 3Vision's Video Markets Tracker puts total streaming revenues at $1.8B in 2026, rising 72% to $3.1B by 2031, the highest growth rate of any region covered in the forecast.

- YouTube is the region's real streaming giant. At $583M in AVOD revenues in 2026, YouTube generates more streaming revenue than any individual SVOD platform in Sub-Saharan Africa, more than Netflix's entire subscription business outside South Africa. By 2031 it reaches $1.18B, accounting for 92% of the region's total AVOD pool.

- Netflix dominates SVOD but faces structural monetisation limits. At 6.2M subscriptions growing to 9.6M by 2031, Netflix is unchallenged in scale, but Naira devaluation in Nigeria and low ARPUs across the region mean subscription revenue growth consistently lags subscriber growth.

- Showmax's shutdown in April 2026 removed the region's only scaled local SVOD challenger after an eleven-year, $522M experiment. Its exit reshapes the competitive layer without changing the region's underlying economics.

- A new generation of Nollywood-native platforms (Kava, EbonyLife ON Plus and Circuits) is experimenting with hybrid pricing, cinema-first releases and diaspora distribution rather than the pure SVOD model that has repeatedly failed in Nigeria.

Sub-Saharan Africa Streaming Revenue: A Region Built on AVOD, Not SVOD

Sub-Saharan Africa does not look like any other streaming market. 3Vision's Video Markets Tracker, covering platform-level SVOD, AVOD, FAST, TVOD and EST forecasts across seven global regions, puts the region's total streaming revenue pool at $1.8B in 2026, rising to $3.1B by 2031.

SVOD accounts for 58% of streaming revenues in 2026 and AVOD accounts for 35%, a far more balanced split than in any Western market. By 2031, AVOD grows 103% to $1.3B while SVOD grows 59% to $1.6B, converging rather than diverging. This is not a market transitioning from subscription to advertising. It was always going to be advertising-first for most consumers, with subscription layered on top for a smaller, wealthier segment.

SVOD subscriptions grow 60% over five years, from 11.0M in 2026 to 17.6M by 2031, while unique subscribers rise from 6.8M to 10.0M, with stacking increasing from 1.62 to 1.76 subscriptions per subscriber. Mobile-first consumption underpins both dynamics: mobile SIM subscriptions reach 1.25 billion in 2026, while fixed broadband lines grow 26% to 12.6M by 2031.

For operators, the implication is clear. Sub-Saharan Africa rewards platforms that can monetise through advertising at scale while building subscription as a secondary engine, not the reverse.

In global context, Sub-Saharan Africa's 35% AVOD share of streaming revenue stands out sharply. North America and Western Europe remain overwhelmingly subscription-led, with AVOD typically below 20% of the streaming revenue pool. For investors and content distributors evaluating market entry, the data underscores that revenue strategies proven in mature markets will not transfer directly to this region without significant adaptation toward ad-supported and hybrid monetisation models.

Nigeria Streaming Market: YouTube AVOD Revenue Surpasses Netflix SVOD

Nigeria is the region's clearest evidence of YouTube's dominance. YouTube generated $128M in advertising revenue there in 2026, growing to $279M by 2031, more than Netflix's entire SVOD business across the rest of Sub-Saharan Africa outside South Africa.

The subscription market, meanwhile, remains structurally difficult. Showmax shut down in April 2026 having lost hundreds of millions over a decade. IROKOtv, once dubbed the "Netflix of Africa", spent over $100M before exiting in 2023. Amazon Prime Video stopped commissioning African originals in January 2024, and Netflix has quietly scaled back Nollywood commissions as Naira devaluation squeezes local ARPU. SVOD revenues grow 60% in Nigeria while subscriptions grow 55%, leaving almost no room for ARPU expansion. Netflix remains the clear leader at 1.2M subscriptions growing to 1.9M, with Amazon scaling from 0.5M to 0.8M.

A new wave of Nollywood-native platforms is building around different economics instead. Kava, launched in August 2025 by Inkblot Studios and Filmhouse Group, runs a cinema-first, diaspora-focused model at ₦1,500/month domestically and $5.99 internationally. EbonyLife ON Plus, launched by Mo Abudu in November 2025, operates as a membership ecosystem at $10/year blending streaming with podcasts and fashion commerce. Neither is trying to out-Netflix Netflix; both are betting that Nollywood's economics (theatrical windows, diaspora reach, hybrid pricing) are a better fit than pure SVOD.

Nigeria's streaming trajectory illustrates a broader pattern across emerging markets: platforms relying solely on subscription revenue face structural headwinds from currency volatility, low disposable incomes and payment infrastructure gaps. The platforms gaining ground are those building around advertising, transactional models and diaspora distribution rather than competing for the same subscription wallet that Netflix and Amazon already occupy.

South Africa Streaming Market: SVOD Subscriptions, Showmax Closure and Platform Competition

South Africa remains the region's dominant market on every measure, with SVOD subscriptions rising from 4.5M in 2026 to 6.8M by 2031 and streaming revenues growing from $530M to $767M.

Showmax's April 2026 closure, after an eleven-year, $522M investment, reshapes the platform stack here more than anywhere else, with its content migrating to DStv Stream outside the streaming dataset tracked by 3Vision. Netflix is the clearest beneficiary, reaching 2.5M subscriptions by 2031; Amazon grows from 1.0M to 1.5M and Disney+ from 0.7M to 1.1M. A notable growth story is Viu, the Canal+-backed platform that doubles from 0.7M to 1.4M subscriptions as K-drama and regional content gain ground alongside Western catalogues in South Africa's increasingly diverse OTT landscape. Following this seismic shift, it will be interesting to see how the consolidated Canal+ and DStv Pay TV businesses address Streaming, and how their approach may evolve.

On advertising, YouTube generates $191M in South Africa in 2026, growing to $325M by 2031, and FAST has more traction here than anywhere else in the region ($3.1M to $10.7M) thanks to more developed connected TV infrastructure.

South Africa's position as the region's anchor market reflects its comparatively higher broadband penetration, stronger digital advertising ecosystem and established pay TV infrastructure. With Showmax's exit, the competitive landscape has simplified around a handful of global SVOD platforms and YouTube's advertising dominance, making South Africa the clearest test case for whether subscription stacking and connected TV adoption can drive the next phase of revenue growth in Sub-Saharan Africa.

East Africa Streaming Forecast: Kenya, Tanzania and Uganda SVOD Growth to 2031

Across Kenya, Tanzania and Uganda, SVOD subscriptions grow from 1.2M in 2026 to 2.1M by 2031, with combined revenues nearly doubling from $189M to $374M.

Kenya leads, reaching 0.8M subscriptions and $175M by 2031, helped by stronger broadband, high smartphone adoption and mobile money penetration via M-Pesa. Kenya is the only Sub-Saharan Africa market outside South Africa projected to surpass 10% SVOD penetration of TV households by 2031. Tanzania and Uganda follow at smaller scale, with AVOD and SVOD revenues converging by 2031 in both markets as YouTube's advertising growth outpaces subscription. Across all three, penetration remains below 10% of TV households. This is a market still being created, not yet being fought over.

For content owners and distributors, East Africa represents the region's most significant untapped opportunity. Low current penetration combined with rapid smartphone adoption and mobile money infrastructure (particularly M-Pesa in Kenya) creates conditions for accelerating SVOD uptake once pricing and content localisation align with consumer spending power.

YouTube Africa AVOD Revenue: The Region's Dominant Streaming Platform

In any other region, SVOD platform dynamics would dominate the streaming story. In Sub-Saharan Africa, YouTube dominates everything.

YouTube generates $583M in AVOD revenues across the region in 2026, growing to $1.18B by 2031. That figure is larger than the total SVOD revenues of every Sub-Saharan Africa market except South Africa, and by 2031 YouTube accounts for 92% of all AVOD revenue in the region. This is not market immaturity; it is structural. With 1.25 billion mobile SIMs in circulation and smartphones as the primary screen, advertising is the natural monetisation pathway for most consumers, and YouTube's free, mobile-first model fits that reality better than any subscription platform can.

As Netflix and Amazon have pulled back on African commissions, YouTube has also become the default distribution channel for a new wave of lighter, cheaper local productions, even though CPMs in Nigeria hover around $1.00. Beyond YouTube, the rest of the region's AVOD market is small ($47M growing to $99M by 2031), and FAST remains nascent outside South Africa. The region's real advertising story is not AVOD in the Western sense. It is YouTube, and the open question is whether anything can build a second advertising engine alongside it.

YouTube's dominance of Sub-Saharan Africa's advertising revenue reflects the structural alignment between its free, mobile-first model and a consumer base where 1.25 billion mobile SIM connections far outstrip the 12.6M fixed broadband lines forecast by 2031. For media companies and advertisers, YouTube is not merely one channel among several in this region; it is effectively the entire addressable video advertising market outside pay TV, and any competitor seeking to build AVOD scale will need to differentiate on content verticals or local-language programming rather than competing on reach.

Sub-Saharan Africa Streaming Outlook 2026-2031: What Operators, Investors and Content Owners Should Expect

Sub-Saharan Africa's streaming market is being built on two engines at once: subscription and advertising scaling in parallel, not sequentially. The platforms that can operate both will define the region's next phase.

Showmax's exit and the emergence of Nollywood-native alternatives show that the pure-SVOD playbook does not transplant cleanly into this market. Netflix, Amazon and Disney+ own global SVOD; Canal+ owns Pay TV infrastructure; YouTube owns advertising. The real question for the next five years is whether anything can grow in the space between them, or whether YouTube's advertising advantage simply keeps compounding.

Taken together, the data from 3Vision's Video Markets Tracker points to a region where the competitive dynamics differ fundamentally from every other market. Revenue growth of 72% over five years will attract new entrants and increased investment, but the winners are unlikely to be platforms replicating Western subscription models. The operators best positioned for the next phase are those building hybrid revenue stacks that combine advertising, transactional and subscription income, with content strategies localised at the country level rather than treating Sub-Saharan Africa as a single market.

All data in this forecast comes from 3Vision's Video Markets Tracker, which covers SVOD subscriber, streaming revenue, AVOD, FAST, TVOD and EST forecasts across Sub-Saharan Africa and six other global regions, with platform-level and country-level detail to 2031. To access the full dataset, request competitive benchmarking or schedule a walkthrough of the forecast, contact 3Vision.

.svg)