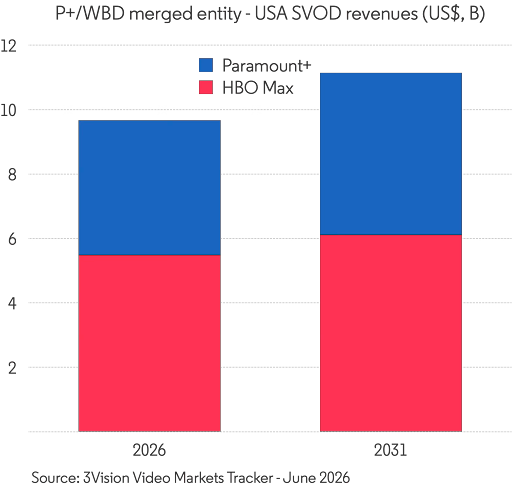

- United States SVOD forecast: 85.8M combined Paramount+ and HBO Max subscriptions in 2026, rising to 91.2M by 2031 (+6%)

- Combined streaming revenue $11.75B, reaching $13.47B (+15%)

- Canada streaming market: Paramount+ at 3.9M subscriptions in 2026, rising to 4.5M by 2031

- HBO Max has no direct Canadian presence - content licensed exclusively to Bell Media's Crave (5.4M subs, growing to 6.3M)

- Global OTT footprint: 200M+ paid SVOD subscribers (HBO Max ~150M, Paramount+ ~80M) plus ~80M Pluto TV FAST MAUs - a ~280–300M combined streaming user base

Key Findings: Paramount-WBD Combined Streaming Footprint and Integration Risk

With the Paramount–WBD merger set to close in Q3 2026, data from our Video Markets Tracker suggests the combined entity will become a credible top-three US streamer almost overnight. But the integration carries $79B of pro forma debt against ~$3B of annual free cash flow, putting unusual pressure on the $6B synergy target. Aggressive cost-cutting isn't optional - it's a debt service requirement.

The most relevant precedent for what happens next isn't Disney/Fox or AT&T/Time Warner. It's Paramount's own absorption of Showtime, which saw 20.5M US subscribers in 2021 fall to zero by 2024. The same management team is now inheriting HBO.

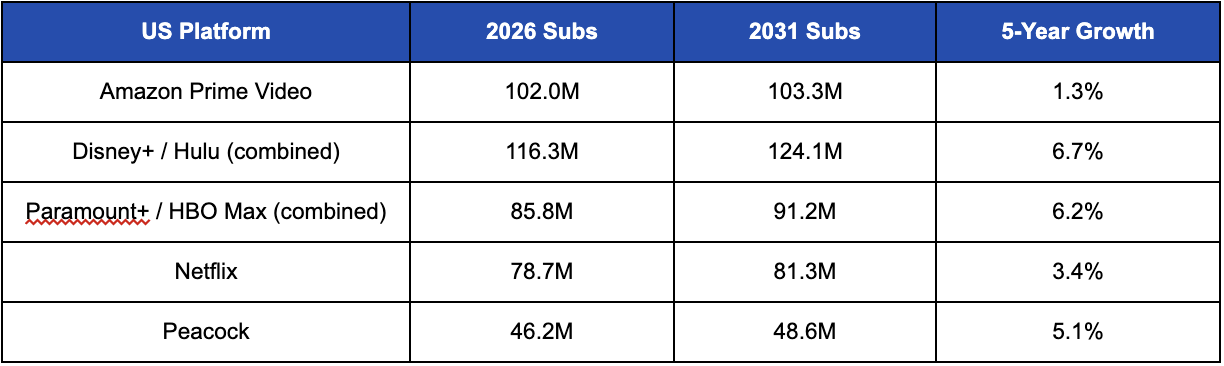

The new combined US footprint is large but slow-growing. Our pre-merger predictions were that Paramount+ would grow its US subscriber base by less than 3% over the next five years, while HBO Max would grow 10% in the same time period. That's 6% growth when combined - shy of Disney+/Hulu's 7% and trailing Amazon Prime Video by ~12M subs in 2031. Scale is achieved. Growth momentum is not.

The ad tier is where the real story sits. Combined ad-supported subscriptions rise from 27.8M to 33.7M in the US - roughly a third of the base. Add Pluto TV's ~80M FAST MAUs and the merged entity's ad-supported reach approaches the scale of YouTube's premium ad inventory. This is the strongest synergy case, and the one most likely to survive integration friction.

The Canadian market situation is genuinely under-discussed. Paramount now owns both Paramount+ Canada and the HBO content licensed to its biggest premium-tier competitor, Crave. There is little strategic logic to this contractual position holding for long.

Deal Terms, DOJ Approval and the Showtime Brand Integration Precedent

Our forecast tracks the Showtime collapse in numbers: 20.5M US subscribers in 2021, 17.4M in 2022, 12.3M in 2023, zero from 2024. The standalone app shut in April 2024. The "Paramount+ with Showtime" tier - pitched at launch as the cornerstone of premium integration - was retired and rebranded back to "Paramount+ Premium" 18 months later. Showtime Sports closed. Productions were cancelled. A premium brand built since 1976 was effectively dismantled inside 24 months.

The same management team now inherits HBO. Ellison's public commitment is that "HBO should stay HBO"; kept editorially independent under Casey Bloys, much as Hulu sits inside Disney+ today as a content tile. It’s a reassuring integration philosophy, but when read against the Showtime data, it's the same promise that was made before.

This is the single most important variable in modelling the post-merger trajectory. If HBO follows the Showtime path, our 91.2M 2031 subscriber forecast overshoots meaningfully. If it doesn't, the $6B synergy target probably doesn't get hit either. If you're an investor, a content partner or talent evaluating the commitment to preserve HBO as an independent editorial brand, this tension defines the deal's risk profile. The Showtime track record is the baseline to model against, not an outlier to dismiss - and the speed of brand dissolution (under 24 months from strategic commitment to full retirement) suggests the window for course correction is shorter than most integration timelines assume.

David Ellison's Streaming Strategy: HBO Max, Paramount+ and 200M+ Global SVOD Subscribers

Pre-merger, the Ellison playbook is already visible. Paramount+, Pluto TV and BET+ are being consolidated onto a single backend infrastructure ahead of the WBD close - likely a rehearsal for absorbing HBO Max under the same architecture.

What sits inside that architecture after close is enormous. HBO Max passed 140M paid global subscribers in Q1 2026 and is targeting 150M by year-end. Paramount+ sits at ~80M globally. That's the 200M+ figure cited at the deal announcement. Layer on Pluto TV's ~80M MAUs, plus smaller paid footprints at BET+ and discovery+, and the total user touchpoint count lands in the 280–300M range — a free-and-paid reach matched only by Amazon and YouTube.

In the US, across HBO Max, Paramount+ and Pluto TV, our Video Markets Tracker forecasts:

- Combined SVOD subscriptions: 85.8M (2026) → 91.2M (2031), +6.2%

- Combined total users: 128.9M → 131.8M, +2.2%

- Combined SVOD revenue: $9.67B → $11.14B, +15%

- Combined AVOD revenue: $3.51B → $4.05B, +15%

- Hybrid (ad-supported) subscriptions: 27.8M → 33.7M, +21%

.png)

For the broader market, this ad-tier trajectory signals a structural shift. The combined entity will likely push harder on revenue per subscriber across the merged portfolio, making ad-supported monetisation - not subscriber acquisition - the primary growth engine through 2031. That pivot from volume to yield is already visible in how Disney+ and Netflix have repriced their own ad tiers over the past 18 months. But the combined Paramount-WBD ad inventory at scale could make this the most significant new entrant in connected TV advertising since Peacock launched its ad-supported model.

If you're buying or planning TV advertising, the consolidation of Paramount+, HBO Max and Pluto TV ad stacks onto a single programmatic infrastructure creates a reach proposition that simply didn't exist outside big tech platforms before.

US SVOD Subscriber Forecast 2026–2031: Paramount+ and HBO Max Combined vs Netflix, Disney+ and Amazon

Paramount+ grows just 2.7% in the US over five years. HBO Max grows 10%. Combined, they sit behind Disney+/Hulu by ~33M subs in 2031 and behind Amazon by ~12M.

This matters for the synergy case. $6B in cost synergies on a slow-growth subscriber base is a fundamentally different proposition than $6B on a high-growth one. There's less revenue uplift to absorb integration friction, churn from app migrations or content cancellations. And the combined US forecast represents an upper bound - when two platforms with overlapping audiences merge, bundle stacking compresses the subscriber count rather than expanding it. The real 2031 number is likely lower than 91.2M, not higher.

The takeaway: Paramount-WBD doesn't have a subscriber-led growth story to offset integration risk. The path to value creation runs through revenue per subscriber, pricing power and ad monetisation - all of which are harder to deliver if HBO's premium brand identity gets diluted the way Showtime's did. If you're benchmarking this against the Disney+/Hulu integration or Amazon's MGM absorption, the key watchpoints are 1) whether subscriber churn accelerates during the app migration window and 2) whether the merged platform can hold per-subscriber economics while folding two pricing structures and content libraries into one product.

Canada Streaming Market: How the Paramount-WBD Merger Threatens Crave's HBO Licensing Deal

HBO Max has zero direct Canadian presence. Warner's premium content is exclusively licensed to Bell Media's Crave through an output deal Bell renewed in October 2024 on multi-year, undisclosed terms. Bell publicly confirmed the agreement remains in place "for the foreseeable future" after the Paramount deal was announced, but this can’t hold forever.

Paramount now owns both Paramount+ Canada - 3.9M subscribers in 2026, growing to 4.5M by 2031 in our forecast - and the HBO content powering its biggest premium-tier competitor. Crave's value proposition is built substantively on HBO. We track Crave from 5.4M to 6.3M subscriptions across the period, but that trajectory implicitly assumes the WBD output deal renews on broadly similar terms.

At the next renewal, Paramount has three options. Renew on existing terms and keep subsidising a Canadian competitor. Renew aggressively and capture more of the value. Or pull HBO content back and either fold it into Paramount+ Canada or launch HBO Max Canada directly to align with the global app rollout.

The third option is the only one consistent with the broader integration strategy. If you're consolidating four streaming services onto a single global tech stack to drive $6B in synergies, running HBO Max as a third-party content licence in one of your more valuable markets makes no strategic sense. Crave's forecast trajectory is more fragile than it looks.

If you're a content distributor or broadcaster in other markets where HBO Max operates via third-party output deals - parts of Europe, Asia Pacific - you should be modelling the same scenario. When a single parent company controls both a domestic streaming platform and the premium content powering a competitor's service, the licensing economics eventually tip toward vertical integration.

Netflix vs Paramount: How the Alternative WBD Bid Would Have Changed the Streaming Landscape

What if Netflix were to have won their initial bid? It is worth quickly running the counterfactual because it isolates which integration risks are deal-specific and which are structural.

The bigger differences sit on the cost side. The Netflix structure excluded WBD's Global Linear Networks, meaning a cleaner streaming-only asset and materially lower combined debt. The pressure to cut aggressively into HBO's content and brand investment to service $79B of debt wouldn't have existed at the same intensity. The synergy maths would have been less punitive.

On brand handling, Netflix's track record looks meaningfully better. Netflix has grown through content acquisition and output deals - Sony, Disney's kids' library, NBCUniversal animation - without acquiring and dismantling competing premium brands. There's no Netflix equivalent of Paramount swallowing Showtime. The likeliest integration path would have been HBO Max content folded into Netflix as an editorial label, closer to how Sony Pictures Television content currently sits inside Netflix than to what happened to Showtime.

For Crave, the Netflix outcome would have been worse, faster. Netflix's existing ~9M Canadian subscribers vastly outweigh Crave's ~4.3M, and the commercial logic of pulling HBO content directly into Netflix Canada would have been irresistible at the next renewal window.

The counterfactual frames the trade-off cleanly. Netflix winning would have meant lower brand destruction risk and lower debt pressure, but a real probability of no deal at all. Paramount winning means the deal closes - but with the management team whose most recent comparable integration is the Showtime data point. The integration approach over the next 18 months tells the rest of the story. For the broader M&A cycle now unfolding across the global streaming industry, this outcome sets a precedent: scale and certainty outweigh brand stewardship in how streaming mega-deals get done.

All data in this analysis comes from our Video Markets Tracker — the platform-level forecast covering SVOD subscriptions, streaming revenue, AVOD, FAST, TVOD and EST across North America, Latin America and five additional global regions through 2031. For the full Paramount–WBD combined dataset, competitive benchmarking against Netflix, Disney+ and Amazon, or a walkthrough of our methodology, get in touch.

.jpg)

.jpg)

.svg)