South Korea's streaming market is worth $3.93bn in 2026 and forecast to reach $5.41bn by 2031, according to 3Vision's Video Markets Tracker - making it one of Asia Pacific's most competitive SVOD and AVOD arenas. Coupang Play is emerging as one of its most strategically distinctive platforms.

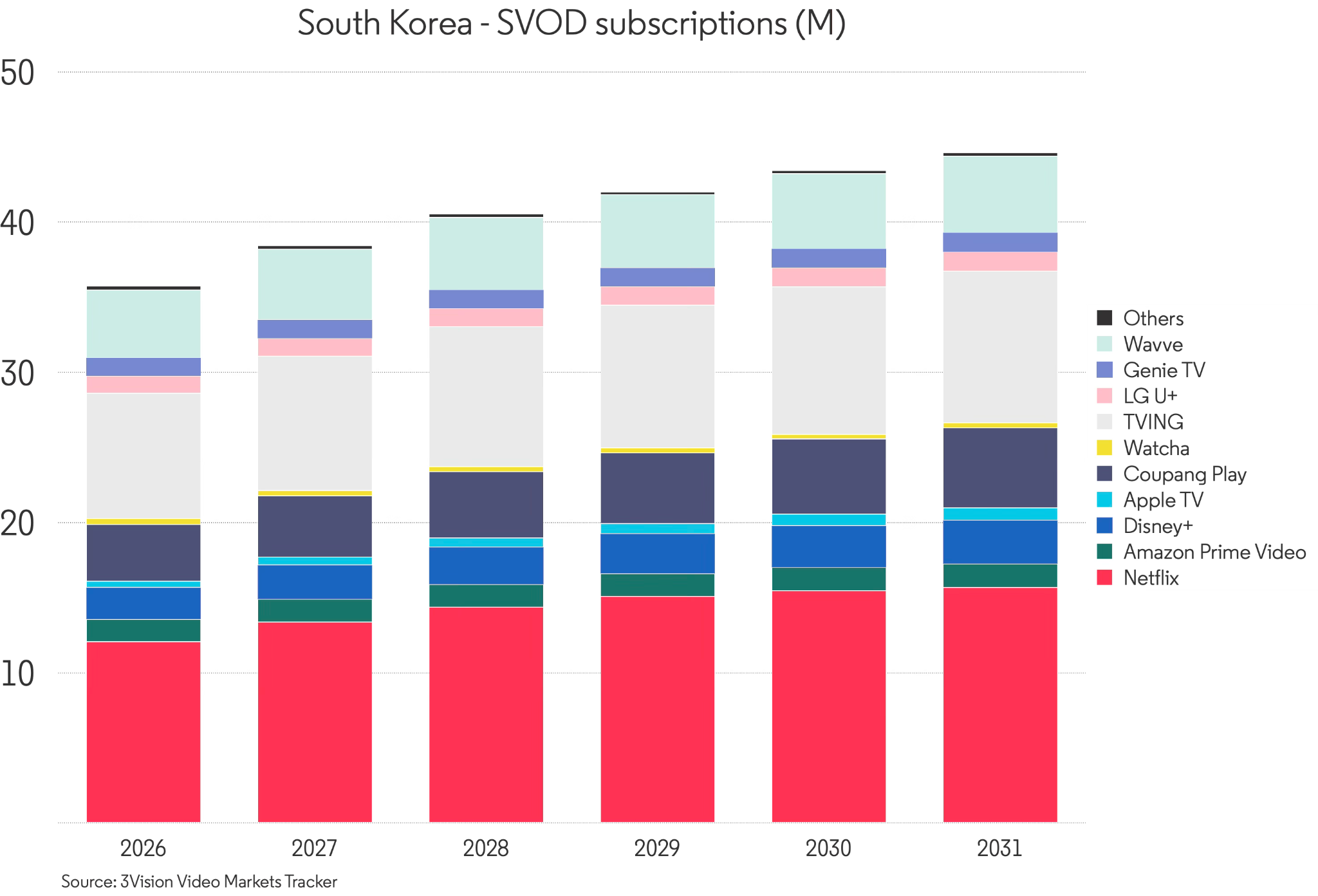

- South Korea's total streaming revenues reach $3.93bn in 2026, with SVOD accounting for 55.8% of that figure

- The market holds 35.8 million SVOD subscriptions in 2026 - 1.70 subscriptions per TV household, reflecting high multi-platform behaviour

- Netflix leads with a 33.8% subscription share, generating $767m in SVOD revenues in 2026

- TVING is the dominant domestic platform with 23.3% subscription share and $714m in revenues, well ahead of Wavve at 12.7% and $130m

- Coupang Play holds 10.6% of SVOD subscriptions in 2026 with 3.8 million subscribers, and its revenues have grown at a 64% CAGR since 2021

- In the past year, Coupang Play premiered 35 acquired titles - more than any other service in South Korea - with Warner Bros. Discovery accounting for 22 of them

SVOD Market Share in South Korea: Netflix, TVING, Wavve and Coupang Play

South Korea’s subscription market is genuinely crowded. At 1.70 SVOD subscriptions per TV household, consumers are stacking services at a rate that rivals more mature Western markets. Netflix sits at the top with a third of all subscriptions and revenues that reflect both scale and pricing power. Below it, TVING - the CJ ENM-controlled platform - has consolidated into the clear domestic leader, with 8.3 million subscriptions and $714m in revenues in 2026, built on a deep catalogue of Korean drama and entertainment alongside live sports and news. Wavve, the joint venture between terrestrial broadcasters KBS, MBC and SBS and telecoms operator SK Telecom, holds 4.5 million subscriptions but generates only $130m in revenues - a mismatch that speaks to structural pricing weakness relative to its subscriber base. The approved merger of TVING and Wavve, which received FTC clearance in mid-2025, will reshape the domestic competitive picture significantly - but as of mid-2026, the two platforms continue to operate independently.

South Korea's 1.70-subscription stacking rate places it among the most competitive SVOD markets in the Asia Pacific region, with growth now driven by tier upgrades and ARPU expansion rather than new household penetration. The Wavve revenue gap signals that pricing discipline, not subscriber volume, will increasingly separate winners from losers as the TVING–Wavve merger compresses the domestic field.

That gap in revenue efficiency is where Coupang Play's story starts to look distinctive.

Coupang Play: Subscriber and Revenue Growth, 2021–2031

Coupang Play launched in December 2020 as the streaming arm of Coupang, South Korea's dominant e-commerce group - a company with roughly 24 million active customers, covering close to half the country's adult population. The strategic logic was familiar: use an existing customer base to accelerate subscription growth, bundle entertainment with commerce, and build engagement across the Coupang ecosystem. Coupang Play is included as part of the company's Rocket WOW membership, which also covers its signature rapid delivery service.

What has followed is harder to dismiss than that origin story might suggest. From 797,000 subscriptions in 2021, Coupang Play has grown to 3.8 million by 2026 - a 37% CAGR - and 3Vision's VMT forecasts put it at 5.3 million by 2031. Revenue growth has been even steeper: from $8m in 2021 to $96m in 2026, a 64% CAGR, with the trajectory projecting toward $172m by 2031. The revenue CAGR outpacing subscriber growth indicates meaningful ARPU expansion and bundle-driven monetisation - positioning Coupang Play as a structurally significant distribution endpoint for studios seeking secondary windows in South Korea.

Coupang Play's HBO and WBD Content Strategy in South Korea

The revenue acceleration reflects a content acquisition strategy that became dramatically more legible in early 2025. In March of that year, Coupang Play became the exclusive home for HBO and HBO Max original content in South Korea - a significant shift, given that this content had previously been distributed through Wavve. HBO Max has never launched as a standalone service in the Korean market, and with WBD's strategic pivot away from direct-to-consumer launches in certain territories, Coupang Play has emerged as the de facto destination for the studio's premium scripted output.

3Vision's Show Tracker data makes the scale of this relationship clear: of the 35 titles Coupang Play premiered in the past year, 22 were distributed by WBD - making it the single largest content pipeline into the platform. All-time, WBD accounts for 53 of Coupang Play's 78 tracked titles.

The HBO slate gives Coupang Play something that most second-tier services in competitive markets struggle to acquire: marquee scripted programming with genuine appointment-viewing pull. Over the past twelve months, that has meant first-window access to A Knight of the Seven Kingdoms, The Pitt (seasons one and two), IT: Welcome to Derry, Duster, and And Just Like That… season three - alongside titles like The Regime, Get Millie Black, and The Chair Company. These are not filler acquisitions. They are the kind of titles around which a subscriber proposition can be credibly built.

Beyond WBD, Coupang Play has assembled a supporting slate from AMC Networks - primarily The Walking Dead franchise, with six titles across multiple spin-offs premiered in 2025 - alongside NBCUniversal content including Suits: L.A. and The Gilded Age season three, and selected BBC Studios titles such as Death Valley. The platform also carries individual titles from Sony Pictures International Television and Paramount Global Content Distribution, though it is worth noting that much of Sony and Paramount's broader Korean output is funnelled through Coupang Play's segmented add-on content blocks - Sony Pictures Pass and Paramount+ Pass - rather than the core subscription, complicating direct comparisons of catalogue depth. The Paramount+ Pass arrived via a licensing deal struck in late 2024, after Paramount ended its previous distribution arrangement with TVING.

Taken together, the content mix tells a clear story: Coupang Play is building its acquired catalogue around premium US scripted drama, with WBD as the anchor relationship, supplemented by targeted deals with mid-major studios. In a market where TVING's strength is domestic Korean content and Netflix competes on global originals, this gives Coupang Play a recognisable identity - one that is distinctly positioned rather than merely derivative. WBD's decision to consolidate premium output behind a single local partner rather than launch HBO Max directly reflects a wider Asia Pacific pattern, where US studios increasingly favour local platform partnerships over standalone direct-to-consumer launches - a dynamic with implications for content licensing value across the region.

Acquired Content Premieres in South Korea: A Platform Comparison

The Show Tracker data also reveals something counterintuitive about Coupang Play's position in the broader acquisition market. In the past year, it premiered more titles than any other service in South Korea - 35 - ahead of Disney+ and Wavve (23 each), Paramount+ (15), and TVING (10). Netflix, which dominates on subscriptions and revenue, premiered just six acquired titles over the same period.

This disparity reflects the different content strategies at work. Netflix in Korea relies heavily on originals and co-productions; TVING invests in domestic programming; Disney+ leans on its own studio pipeline. Coupang Play, by contrast, is running what is essentially a US acquisition strategy - licensing premium scripted content from multiple studios and positioning itself as the aggregation point for American prestige television. It is a model with clear precedent in other Asian markets, but Coupang Play is executing it at a scale and specificity that sets it apart domestically. For content distributors and production companies, the data signals that Coupang Play is now the most active acquired-content buyer in the South Korean market - and a critical sales channel for studios without their own local platform.

Sports Rights, AVOD and South Korea's First Free Ad-Supported Streaming Tier

Content acquisitions are only one leg of the strategy. Coupang Play has invested aggressively in live sports rights, assembling a portfolio that now includes LaLiga (exclusive digital rights in South Korea from 2023 to 2028), the AFC Champions League and Asian Cup qualifiers (exclusive, 2025–2028), the K League, the Bundesliga, Ligue 1, the English Premier League and FA Cup, the EFL, and Formula 1. This breadth of sports rights is unusual for a platform of Coupang Play's scale and gives it a second axis of differentiation - one that drives engagement among audiences that drama content alone cannot reach.

In June 2025, Coupang Play went a step further, launching South Korea's first free ad-supported streaming tier. Under this model, much of the platform's content - including sports - became available without a subscription, supported by advertising. Rocket WOW members retain ad-free access and premium features. The move positions Coupang Play to capture both subscription and advertising revenue, and the early trajectory is visible in the VMT data: 1.1 million AVOD MAUs in 2026, projected to reach 3.2 million by 2031. The total AVOD market in South Korea generates $1.32bn in ad revenues in 2026, with FAST accounting for 43% of that total. As Coupang Play builds out its advertising infrastructure, its e-commerce parent provides an unusually rich first-party data asset - one that most domestic competitors cannot match. The AVOD launch signals that South Korea's streaming market is now mature enough to support hybrid SVOD/AVOD monetisation - an addressable advertising opportunity that pure-play streamers and domestic broadcasters will find difficult to replicate.

Watcha's Decline and the Squeeze on Mid-Tier SVOD Platforms

The other domestic player that defines Coupang Play's context is Watcha - and its trajectory runs in precisely the opposite direction. Once positioned as South Korea's answer to the subscription curation model, Watcha has shed subscriptions steadily since 2021, falling from 1.29 million to 381,000 by 2026 and revenues from $88m to $17m over the same period. Content investment has been insufficient to retain subscribers against better-capitalised competition, and the path to viability looks increasingly narrow.

The contrast is instructive. Watcha lacked both the financial backing and the content identity to hold its ground. Coupang Play has the backing from its e-commerce parent and has now built a content identity around HBO, US prestige drama, and live sports - a combination that is commercially defensible in a way that Watcha's generalist curation model never was. Watcha's trajectory suggests that mid-tier subscription platforms without either a captive distribution base or a distinctive content moat face structurally narrowing economics - a pattern worth watching across comparable Asia Pacific markets.

South Korea Streaming Market Forecast to 2031

South Korea's total streaming market grows from $3.93bn in 2026 to $5.41bn by 2031 - a 38% expansion driven by continued SVOD penetration and accelerating AVOD monetisation. Within that, the subscription market reaches 44.6 million subscriptions by 2031, with Netflix, TVING, and Wavve all growing in absolute terms. Coupang Play adds a further 1.5 million subscriptions over the same period, reinforcing its position as the fourth domestic platform by size.

The more interesting question is revenue. At $172m in projected SVOD revenues by 2031, Coupang Play will remain well behind Netflix and TVING but will have established a durable, commercially coherent position - one built on differentiated content (HBO and US scripted drama), structural distribution advantages (e-commerce bundling), a deepening sports rights portfolio, and an emerging AVOD capability that its rivals will find difficult to replicate.

South Korea's streaming market rewards platforms that understand what they are for. Coupang Play, unlike several of its predecessors, seems increasingly clear on the answer. The forecast trajectory favours platforms with diversified revenue models - subscription, advertising, sports, bundling - over those relying on a single monetisation lever, and Coupang Play's projected 2031 position illustrates the kind of durable, differentiated platform identity that the South Korean market increasingly demands.

All data in this analysis is sourced from 3Vision's Video Markets Tracker and Show Tracker, which provide subscriber, revenue, MAU, AVOD, FAST, and content acquisition forecasts across South Korea, Asia Pacific and global streaming markets. For platform-level SVOD and AVOD forecasts, title-level content tracking, and competitive intelligence on Coupang Play, Netflix, TVING, Wavve and Watcha, contact the 3Vision team.

.svg)