Asia Pacific Streaming Market Forecast to 2031:

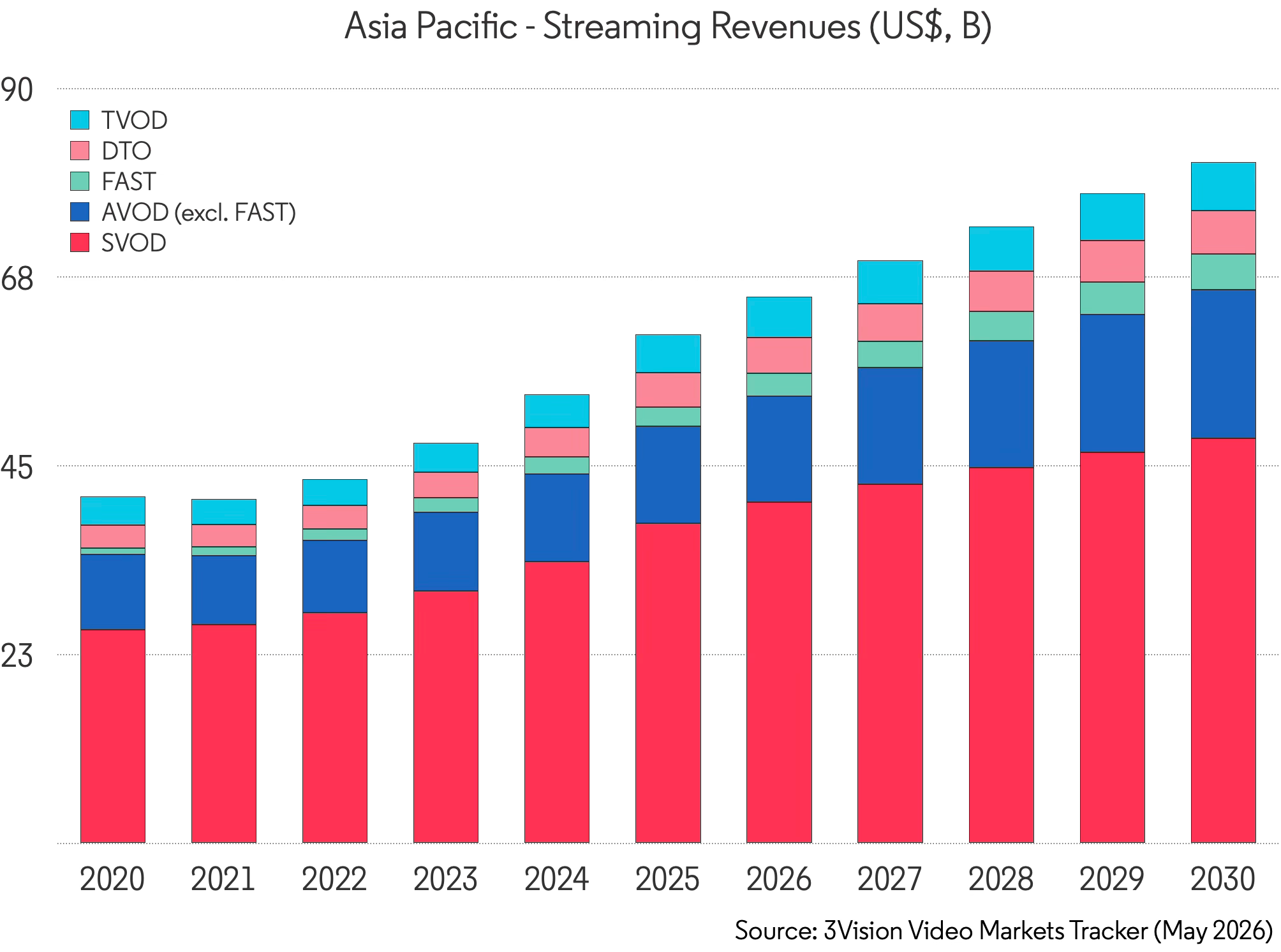

- Total Streaming Revenue 2025: $53.5B

- Total Streaming Revenue 2031: $74.4B

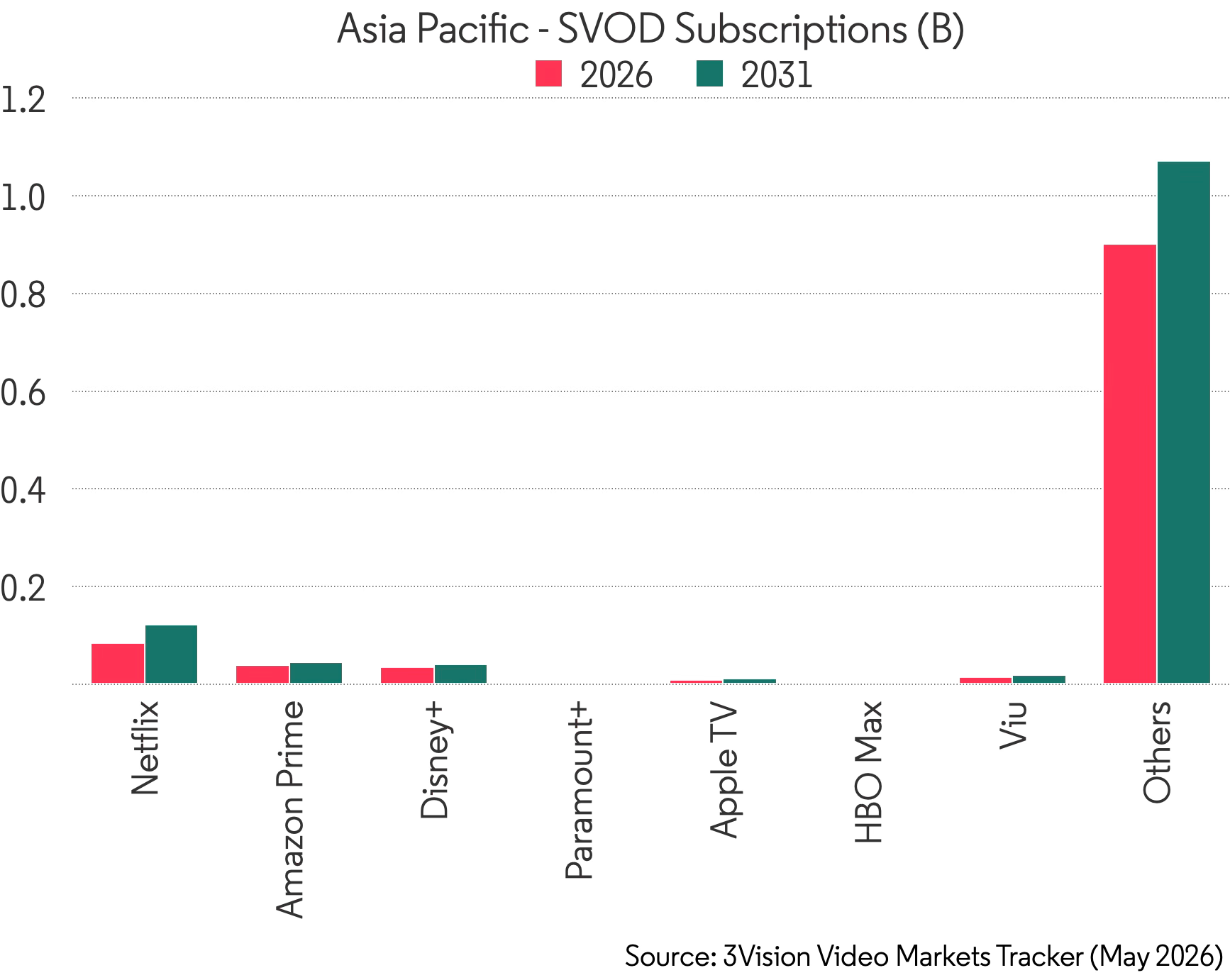

- SVOD Subscriptions 2025: Over 1 Billion

- AVOD Monthly Active Users 2025: 2.76 Billion

- Local and Regional Platforms' Share of Subscriptions: 84%

Key Findings:

- Local and regional platforms hold 84% of SVOD subscriptions across Asia Pacific. Global platforms are competing for the secondary slot in most markets.

- The ad-supported audience dwarfs the subscription base.

- India is the growth engine. Total streaming revenues are forecast to roughly double by 2031, driven by JioHotstar's dominance and a competitive domestic ecosystem of ZEE5, SonyLIV, Amazon and a fast-growing Netflix.

- FAST is the fastest-growing segment across the region, outpacing both SVOD and AVOD - and it is growing fastest in the markets that are least developed today.

According to new data from 3Vision’s Video Markets Tracker, Asia Pacific is the world’s largest streaming market by subscriber volume and the fastest-growing by revenue. With total streaming revenues of $53.5B in 2025 forecast to reach $74.4B by 2031, the scale is not in question. What is less well understood is who is actually winning, which OTT revenue models — SVOD, AVOD and FAST — are growing fastest, and where the real commercial opportunity lies for operators, investors, broadcasters, content owners and media companies over the next six years.

The headline finding is straightforward. Local and regional platforms account for 84% of all SVOD subscriptions across the region. Not because Netflix, Amazon and Disney+ have not invested seriously — all three have meaningful presences — but because audiences across Asia Pacific are already well-served by platforms built specifically for them. In market after market, the primary subscription relationship belongs to a local service. Global platforms are competing for the secondary slot.

For senior executives, investors and content owners, this changes how Asia Pacific should be assessed. The region is not simply a scale story led by global SVOD brands; it is a platform-specific and country-specific streaming market where local services often control the primary customer relationship.

Asia Pacific Streaming Market Data: What the Video Markets Tracker Measures

The Video Markets Tracker measures streaming activity across revenue models, platforms and countries. It covers streaming, Pay TV, SVOD, AVOD, FAST, TVOD and DTO revenues, alongside subscribers, MAUs and ARPU. The Tracker also provides country-level and platform-level forecasts to 2031, allowing market performance to be compared consistently across Asia Pacific and six other global regions.

That matters because Asia Pacific cannot be understood through a single headline revenue figure. The region includes mature, high-ARPU markets such as Japan and South Korea; closed domestic ecosystems such as China; mass-market hybrid models in India; ad-supported growth markets across Southeast Asia; and earlier-stage streaming economies including Pakistan, Bangladesh, Sri Lanka and Cambodia. Country-level and platform-level streaming data is therefore more useful than broad regional averages.

Asia Pacific Streaming Market Overview: Country-Level Differences Across China, India, Japan, South Korea and Southeast Asia

Asia Pacific is not a single market. Japan is a mature, high-ARPU ecosystem where Netflix and Amazon compete alongside deeply embedded local services including U-Next, Hulu Japan and Lemino. South Korea is the most advanced subscription-stacking market in the region, where TVING, Wavve and Coupang Play sit alongside Netflix in a competitive domestic landscape shaped by one of the world’s most influential content industries. China is self-contained entirely: Tencent Video, iQIYI, Youku, Mango TV and Bilibili operate a vast streaming economy closed to outside competition, large enough to account for the majority of total regional revenues on its own.

India sits in a category of its own. The consolidation of JioCinema and Disney+ Hotstar into JioHotstar drove a subscriber surge across the region without precedent in the medium’s history. Southeast Asia adds further complexity: six major national markets at different stages of development, each with its own dominant platforms, content preferences and monetisation dynamics. The fastest revenue growth rates in the region are here, but the growth is primarily ad-supported, FAST-led, and tied to connectivity infrastructure that is still being built.

No single market model applies across Asia Pacific. Operators and investors applying a uniform strategy across markets as structurally different as Japan and Vietnam are likely to misallocate capital. The commercial winners will be those who treat each national market as a distinct competitive environment.

Asia Pacific Streaming Market Comparison by Country and Revenue Model

This comparison highlights the central issue for anyone assessing the Asia Pacific streaming market: revenue growth does not follow the same pattern in every country. Some markets are already defined by subscription stacking; others are still building streaming reach through free, hybrid or advertising-supported access.

India Streaming Market Forecast 2025–2031: SVOD, AVOD and FAST Growth in Asia Pacific’s Fastest-Growing Major Market

India’s total streaming revenues are forecast to roughly double between 2025 and 2031 — the fastest rate of any major market in the region, and by a considerable margin.

JioHotstar sits at the centre of that story. Built around cricket, local-language drama and a tiered pricing structure designed for one of the world’s most diverse consumer bases, it recorded over 500M monthly active users in 2025, making it one of the largest streaming platforms on earth by any measure. But India’s ecosystem extends well beyond a single platform. ZEE5 reaches 117M MAUs and is building scale through its app ecosystem and dedicated FAST channels. SonyLIV benefits from wide device distribution and strong sports rights. Amazon Prime Video holds a substantial subscriber base. Netflix, entering the market seriously only recently, is growing faster here than almost anywhere else in its global portfolio.

The majority of India’s SVOD subscriptions sit on hybrid or free-tier plans, making India as much an ad-supported streaming market as a subscription video market. For global platforms, that means subscriber counts are a poor proxy for commercial value; ARPU, advertising yield and bundling economics matter far more. For content owners and investors, India is less a conventional SVOD expansion market than a test case for hybrid streaming economics at mass-market scale.

China Streaming Market Forecast 2025–2031: SVOD Saturation, AVOD Scale and FAST Revenue Growth

China accounts for the majority of total Asia Pacific streaming revenues, and its platform ecosystem operates entirely independently of the global market. Tencent Video, iQIYI, Youku, Mango TV and Bilibili collectively recorded over 1.6B AVOD monthly active users in 2025. This figure underlines both the scale of Chinese streaming and the dominance of ad-supported consumption even in a market with hundreds of millions of paying SVOD subscribers.

SVOD subscription penetration is approaching saturation in China’s urban centres. The next phase of revenue growth is advertising-led: AVOD growing faster than SVOD, with FAST building rapidly from a lower base. For international content owners, China’s closed ecosystem means the region’s largest single revenue pool remains commercially inaccessible, which makes the growth trajectories of India and Southeast Asia all the more strategically important.

China shows why Asia Pacific streaming analysis needs to separate market size from market accessibility. It is essential to any regional forecast, but its closed platform structure limits the direct opportunity for many international players.

Japan and South Korea Streaming Markets 2025–2031: SVOD Maturity, Subscription Stacking, FAST Revenue and CTV Growth

Japan and South Korea are the region’s most developed streaming markets outside China, characterised by high SVOD penetration, meaningful subscription stacking and fast-growing FAST economies built on strong CTV infrastructure. Japan’s broadband lines reach 90% of TV households; South Korea exceeds 100%.

In Japan, U-Next, Hulu and Lemino hold established household positions alongside Netflix and Amazon, and the market retains notable strength in TVOD, reflecting viewing habits that have been slower to shift to pure subscription. South Korea is the standout stacking market in Asia Pacific: TVING, Wavve and Coupang Play anchor domestic SVOD, Netflix is significant, and consumers routinely hold multiple concurrent services. FAST revenues in South Korea are already among the highest in the region and growing fast, supported by CTV penetration and an advertising market increasingly comfortable with digital video inventory.

Both markets demonstrate that SVOD maturity and FAST growth are not mutually exclusive. High subscription penetration does not remove the need for ad-supported growth; instead, it creates the conditions for CTV, FAST and premium digital video advertising to expand around an established paid streaming base.

Southeast Asia Streaming Market Forecast 2025–2031: AVOD, FAST and Local OTT Platform Growth Across Six Markets

Southeast Asia’s streaming markets share a common structural characteristic: local and regional OTT platforms lead, ad-supported streaming models dominate, and FAST is the fastest-growing revenue segment across the board.

Viu has built a strong position across Malaysia, Indonesia, the Philippines, Thailand and Singapore on the back of Korean Wave content — K-drama and K-pop programming with a loyal paying audience that shows no sign of peaking. WeTV, Tencent’s Southeast Asian vehicle, serves Chinese drama, BL content and Thai originals, with its strongest market in Thailand. In Indonesia, Vision+ reaches 110M monthly active users and Vidio 45M — figures that dwarf their SVOD subscription counts and illustrate the true scale of ad-supported reach in the market. Disney+ holds the largest SVOD subscription share in Indonesia, but local platforms dominate actual viewing time. In Malaysia, Astro’s Sooka adds a strong local dimension alongside Viu, Netflix and Disney+.

Vietnam and the Philippines are among the fastest-growing streaming markets in the region, with revenues forecast to roughly double by 2031 — both primarily AVOD-led, with FAST the fastest-growing segment. For content owners evaluating Southeast Asian distribution, licensing strategies optimised purely for subscription platforms will underperform. Platforms like Viu, WeTV and Vidio are building the audience scale that will eventually attract the premium advertising budgets currently concentrated in linear television.

The Southeast Asian streaming opportunity is therefore less about replicating Western SVOD models and more about building reach, local relevance and advertising scale. For content distributors, the strongest commercial route may come through hybrid licensing, AVOD partnerships and FAST channel strategies that reflect how audiences in these markets already consume video.

Emerging Asia Pacific Streaming Markets: Pakistan, Bangladesh and Early-Stage OTT Growth Opportunities

Pakistan is consistently underweighted in regional streaming analysis. With a population of 230M, a young demographic and a market dominated by ad-supported models, it is one of the more significant early-stage opportunities in Asia Pacific. Netflix leads on SVOD subscriptions alongside Starz Play and iflix, but the larger commercial story is AVOD and FAST, with both growing at double-digit rates.

Markets like Bangladesh, Sri Lanka and Cambodia are more deeply underpenetrated still. Connectivity is the primary constraint, and it is being built. Bangladesh alone has a population of approximately 170M. These markets offer the kind of early-stage growth opportunity that India presented five years ago. The platforms and content owners that establish presence before the competitive landscape consolidates will be best positioned when ARPU and advertising spend begin to scale.

These markets matter because they extend the Asia Pacific streaming story beyond today’s largest revenue pools. For investors, platforms and content companies, Pakistan, Bangladesh, Sri Lanka and Cambodia represent future-facing growth markets where distribution, connectivity and ad monetisation may matter before premium subscription revenues fully develop.

AVOD and FAST Revenue Growth in Asia Pacific: Ad-Supported Streaming, CTV and OTT Monetisation

Across Asia Pacific, AVOD revenues are growing at more than twice the rate of SVOD. FAST is growing faster still, driven by accelerating CTV adoption, broadcaster activation of library content through free linear channels, and in markets like Japan and South Korea, genuine cultural alignment with linear viewing habits.

The numbers make the point clearly. The Video Markets Tracker records approximately 2.76B AVOD monthly active users across Asia Pacific in 2025 against roughly 1.02B SVOD subscriptions. The ad-supported audience is nearly three times the size of the subscription base. In China, the ratio is closer to four to one. In India, JioHotstar’s 500M-plus MAUs sit alongside an SVOD subscriber base a fraction of that size.

Subscriber counts, the metric most commonly reported in Western trade press and global SVOD analysis, significantly undercount the actual streaming audience across this region. For platforms, content owners and advertising buyers, MAU reach, advertising yield and content cost-per-view are the metrics that matter.

This is the core difference between Asia Pacific and many Western streaming markets. Subscription totals remain important, but they do not fully explain audience scale or revenue potential. AVOD and FAST performance are increasingly central to understanding where the next phase of streaming monetisation will come from.

What Asia Pacific Streaming Growth Means for Operators, Investors and Content Owners

For operators, investors and content owners, Asia Pacific requires a broader view of streaming value. Subscriber counts remain important, but they are only one part of the market. In many countries, MAUs, advertising yield, ARPU, bundling economics and content cost-per-view are more useful indicators of commercial potential.

For content owners, this means SVOD licensing alone is unlikely to capture the full opportunity. The strongest distribution strategies are likely to combine SVOD windows, AVOD licensing, FAST channel launches and local platform partnerships. In Japan and South Korea, paid streaming and CTV-supported FAST can sit side by side. In India and Southeast Asia, reach and advertising scale may matter as much as direct subscription revenue. In emerging markets, early distribution may be valuable before premium subscription economics fully develop.

For investors and operators, the same logic applies. A large MAU base does not automatically translate into high ARPU, but it can create long-term advertising and bundling potential. A mature SVOD market does not eliminate growth, but it changes where that growth is likely to come from. The strongest Asia Pacific streaming strategies will be those that evaluate each market on its own terms: who owns the customer relationship, which model is growing fastest, how audiences access content, and whether revenue growth is being driven by subscription fees, advertising or hybrid monetisation.

Key Streaming Terms

Key terms used in this analysis include SVOD, referring to subscription video on demand; AVOD, meaning advertising-supported video on demand; FAST, or free ad-supported streaming television; MAUs, meaning monthly active users; ARPU, meaning average revenue per user; CTV, meaning connected TV; and OTT, referring to video delivered over the internet rather than through traditional broadcast, cable or satellite distribution.

Asia Pacific Streaming Data by Platform, Country and Revenue Model: What 3Vision’s Video Markets Tracker Covers

Asia Pacific rewards specificity. The platforms that matter commercially are not always the ones with the highest global profiles — Vidio in Indonesia, Sooka in Malaysia, TVING in Korea, ZEE5 in India — and the deals that generate durable revenue are often with services operating at national or sub-regional scale, in languages and genres that rarely feature in global trade press.

The platform-by-platform, market-by-market picture — SVOD subscribers, AVOD MAUs, streaming revenues, ARPU, FAST forecasts, AVOD forecasts and competitive dynamics — is considerably more detailed and more actionable than any regional headline conveys.

That is exactly what the Video Markets Tracker is built to provide.

Asia Pacific Streaming Market Outlook to 2031

Asia Pacific’s streaming market outlook to 2031 is defined by three connected trends: local platform strength, ad-supported scale and market-specific monetisation. The region is already the world’s largest streaming market by subscriber volume, but its next phase of growth will not be driven by a single model or a single set of global platforms.

SVOD remains central, especially in mature and high-value markets. But AVOD and FAST are increasingly important to understanding actual audience reach and future revenue growth. In India, Southeast Asia and emerging Asia Pacific markets, hybrid and ad-supported models are central to the commercial story. In Japan and South Korea, mature subscription markets are creating the base for further CTV and FAST expansion. In China, scale remains enormous but structurally separate from the open global streaming economy.

For operators, investors, broadcasters and content owners, the implication is clear: Asia Pacific streaming growth is real, but it is not uniform. The opportunity sits at the intersection of country, platform, business model and audience behaviour.

3Vision’s Video Markets Tracker is the source for the Asia Pacific streaming market data, forecasts and platform analysis in this article. The Tracker covers streaming, Pay TV, SVOD, AVOD and FAST revenues, subscribers, MAUs and ARPU across Asia Pacific and six other global regions — with platform-level and country-level forecasts to 2031. To explore the full Video Markets Tracker dataset or request a demo, visit 3Vision at https://www.3vision.tv/

.svg)