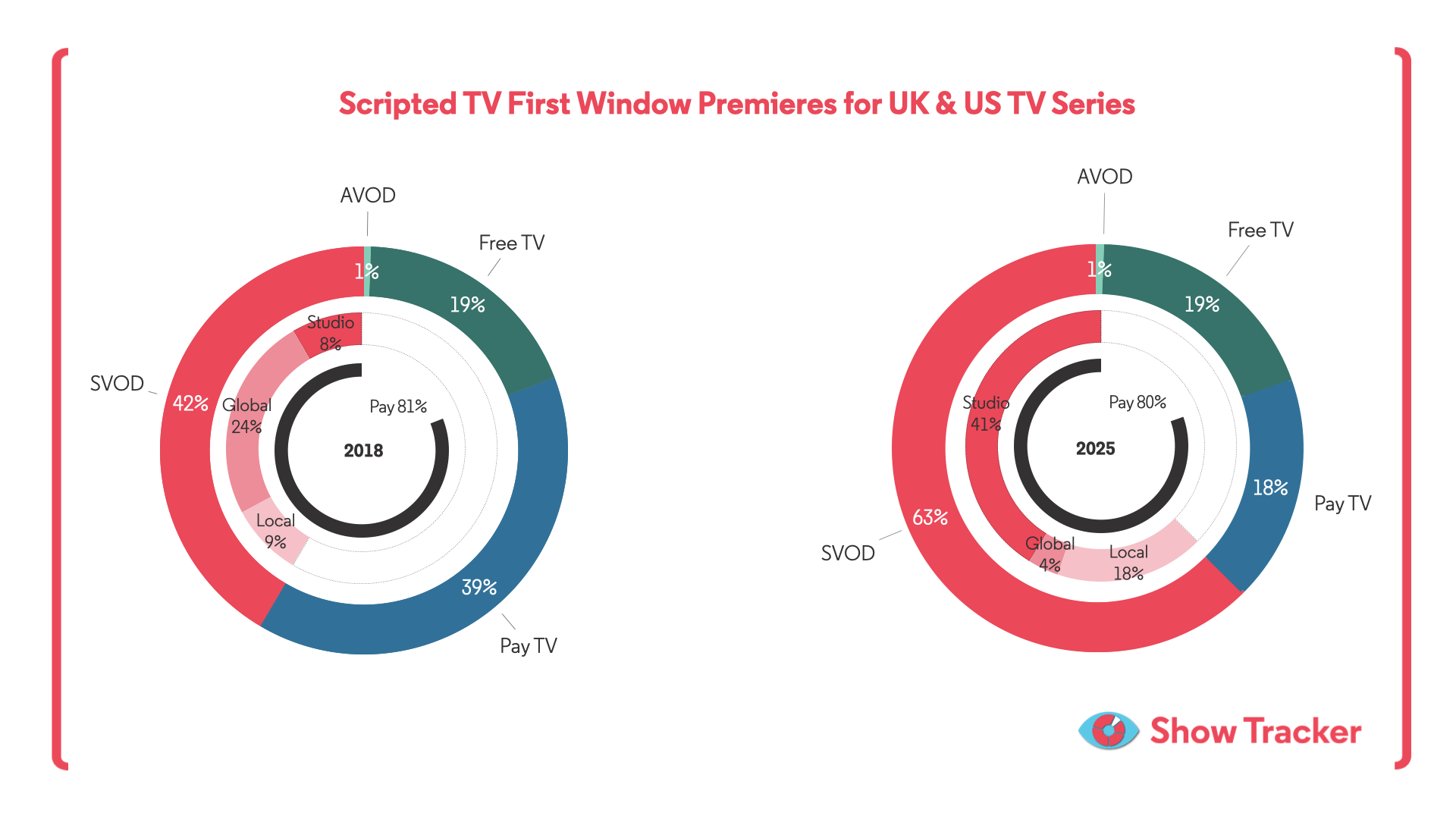

3Vision’s Show Tracker data shows a first window scripted TV market that has changed significantly in shape, but less in how audiences access premium content.

Pay TV is no longer the dominant gateway it once was for new US and UK scripted series. SVOD now plays a much larger role, particularly as major studios have shifted more content onto their own direct-to-consumer platforms.

This has changed where audiences go to watch new drama and comedy premieres. It has also reduced the role of the traditional Pay TV package as the default home for premium scripted content. But it has not removed the paywall.

The main shift has been from one type of paid access to another. Where Pay TV once acted as a centralised route to a wide range of premium scripted series, the market is now spread across a broader mix of SVOD services. Studio-owned SVOD platforms have become more prevalent, leaving Pay TV with a narrower role in the first window market.

In 2018 the likes of Netflix and Amazon were engaging heavily with third-parties in the first window, often acquiring titles for a global release outside the US. As SVOD originals became a larger part of their content strategies, so too did first window acquisitions fall between 2018 and 2025. More recently, however, there have been some signs of renewed acquisition activity from these platforms, especially in second window.

Free TV has held its place, but not without adapting. Broadcasters are increasingly using boxsets and BVOD-first releases to make their services more competitive with subscription platforms. This gives free services a stronger on-demand proposition. But it has not fundamentally shifted first window access away from paid platforms.

The growth of boxset availability on Free TV is still important. It shows broadcasters responding to viewing habits shaped by streaming, where immediate access to full seasons is now familiar. Linear scheduling remains part of the market. But it is no longer enough on its own.

The result is a market that looks transformed at the buyer level, but remains highly consistent at access level. Pay TV has lost share. SVOD has expanded. Studio platforms have become more central. Global SVOD acquisition strategies are evolving again. And broadcasters are leaning further into BVOD and boxsets.

Yet the underlying commercial reality remains largely unchanged. Premium first window US and UK scripted TV is still overwhelmingly subscription-led.

The paywall has not disappeared. It has changed shape.

.jpg)

.jpg)

.svg)