3Vision’s Show Tracker points to a continued slowdown in the third-party distribution of US scripted series across EMEA. Major studios are keeping more of their key titles for their own streaming services, while local buyers are becoming more selective about what they acquire. The result is a market where fewer US scripted series are finding third-party homes.

This is not just a story about studio-owned platforms taking content out of the market. That shift is already well established. Disney has had a direct-to-consumer footprint across EMEA for several years. Paramount has built scale through Paramount+ and SkyShowtime. NBCUniversal has used SkyShowtime alongside its existing relationship with Sky. Warner Bros. Discovery has now followed with HBO Max in the UK, Germany and Italy, bringing the service to all major European markets.

The more revealing question is what happens to the titles that studios and distributors without their own SVOD services, namely those looking to sell to third-parties. The answer is that they are selling less consistently, and less quickly.

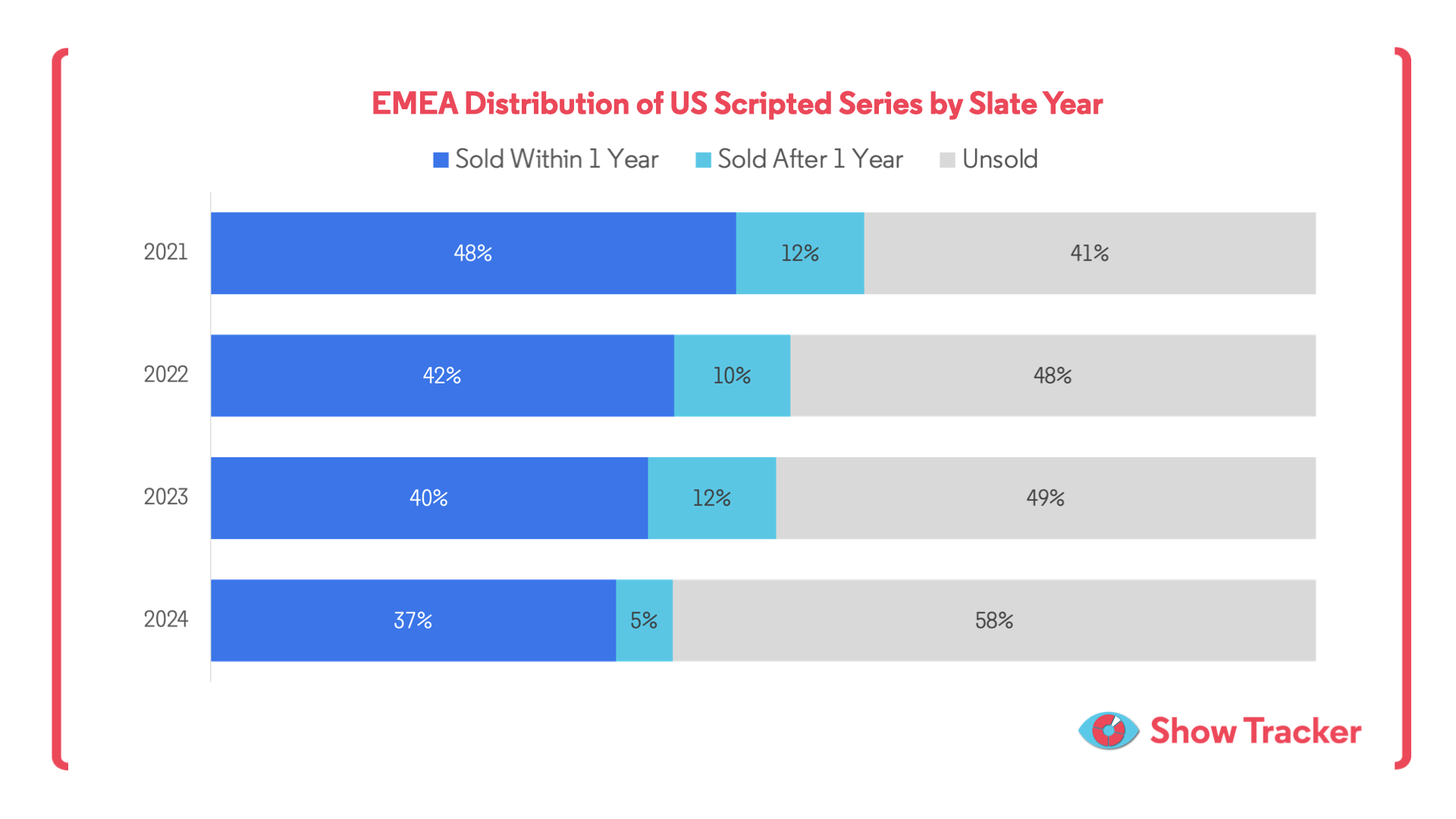

Just under half of the 2021 US scripted slate analysed by Show Tracker was sold in EMEA within one year of launch. By the 2024 slate, that figure had fallen to 37%. Sales after the first year have remained limited, meaning the unsold share has grown. For the 2024 slate, 58% of titles have so far remained unsold across the EMEA markets tracked. This suggests the market is not simply moving from fast sales to slower sales. A growing share of available US scripted series are not being picked up at all.

Two pressures are driving the change. On the supply side, studio-owned SVOD services have reduced the volume of premium US scripted content available to third-party buyers. On the demand side, local broadcasters and platforms - particularly Pay TV and Free TV services - are under greater budget pressure. They are still buying, but they are making fewer early commitments and choosing more carefully.

The genre picture is also becoming more uneven.

Comedy faces the toughest route to market. Across the tracked EMEA territories, comedy titles are selling reliably in only a small number of markets, with Germany, South Africa and the UK standing out as the strongest. Several other major markets show little or no third-party activity for the comedy slate. Drama remains stronger, but the picture is still far from uniform.

For 2024 drama titles, the only tracked markets where more than half the slate has found a home are the UK, Spain, South Africa, Italy and Germany. The UK is the clear outlier, with 65% of the 2024 US drama slate sold within one year and a further 9% sold after one year. Germany also remains strong, with 63% sold within one year. South Africa, Spain and Italy show relatively robust demand too, but several other markets remain much more selective.

Traditional local broadcasters are still acquiring US scripted content, but budget constraints mean they are becoming more cautious about first-window deals. In some cases, Free TV buyers are entering later, after a title has already debuted on a studio SVOD service, either as as second window or a library deal. These deals may also be non-exclusive, with the same title remaining available on the studio platform while airing on a local broadcaster.

The strongest opportunities are clustered around drama and around markets that continue to show clear appetite for US scripted content, particularly the UK, Germany, South Africa, Spain and Italy. Comedy faces a narrower path, with demand concentrated in fewer territories. For now, selectivity is the new normal.

.jpg)

.jpg)

.svg)