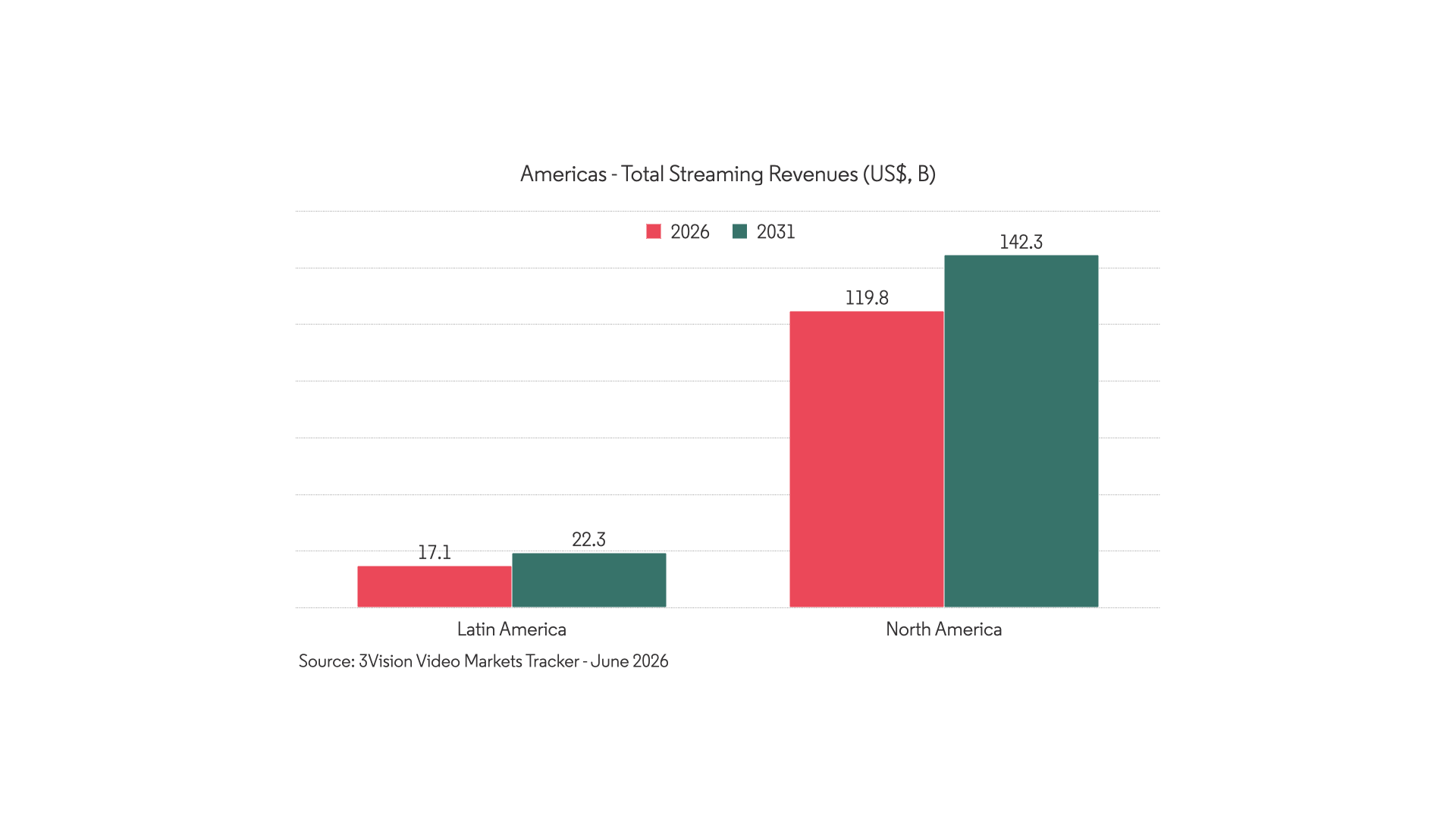

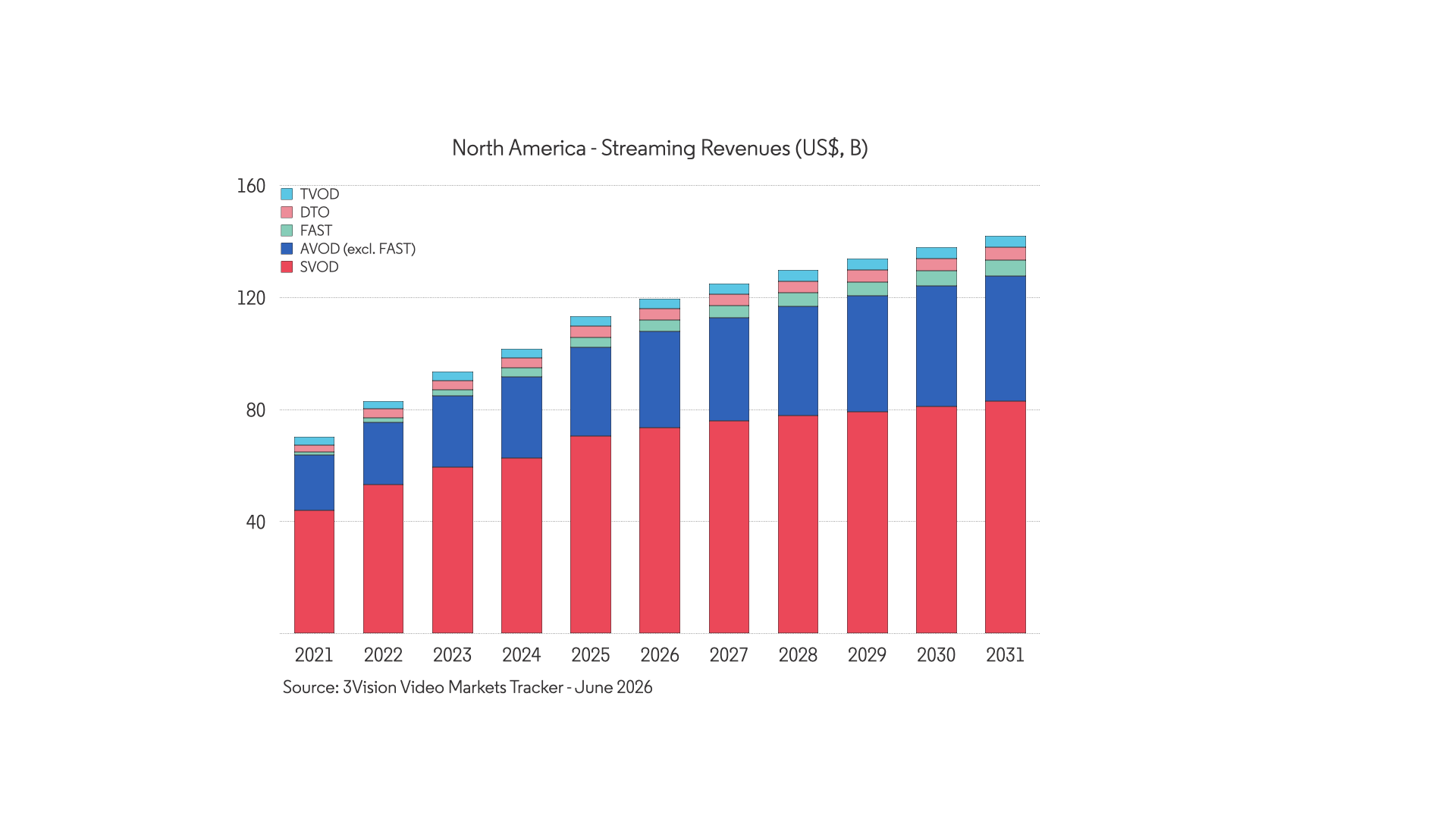

North America: 527M SVOD subscriptions in 2026, rising to 551M by 2031 (+4%) | Total streaming revenues $119.8B, reaching $142.3B (+19%)

Latin America: 142M SVOD subscriptions in 2026, rising to 178M by 2031 (+25%) | Total streaming revenues $17.1B, reaching $22.3B (+31%)

Combined Americas: 669M SVOD subscriptions | $136.9B in total streaming revenues in 2026, reaching $164.6B by 2031

Key Findings:

- The Americas are the world's largest streaming market by revenue — and the gap is widening. Our Video Markets Tracker puts combined streaming revenues across North and Latin America at $164.6B by 2031, with the US alone generating $133B. But the two halves of the hemisphere are growing for very different reasons.

- North America is a consolidation story. The pending Paramount–WBD merger will create a 200M+ subscriber platform, reshaping the competitive layer below Netflix and Disney. Scale is becoming existential.

- Latin America is still an expansion story. SVOD subscriptions grow 25% - six times faster than North America - driven by broadband rollout in Colombia, Brazil and Mexico.

- Live sports are now baked into streaming economics across the hemisphere. Amazon's NBA package, Netflix's five-game NFL deal, Apple's exclusive Formula 1 rights, ESPN Unlimited's standalone launch and the FIFA World Cup 2026 across the US, Canada and Mexico make sports the single most important retention and acquisition lever in the Americas.

- Ad-supported streaming is the fastest-growing revenue segment in both regions. North American AVOD grows 32% to $50.3B. Latin American AVOD grows 74% to $8.0B. Hybrid tiers are mainstream, not peripheral. In Brazil, AVOD already accounts for 37% of total streaming revenue.

North America vs Latin America: Two Halves of a Hemisphere

The Americas contain both the world's most mature streaming market and some of its fastest-growing ones. Our Video Markets Tracker - covering platform-level SVOD, AVOD, FAST, TVOD and EST forecasts across seven global regions - puts the combined streaming revenue pool at $136.9B in 2026, rising to $164.6B by 2031. But the dynamics in each half couldn't be more different.

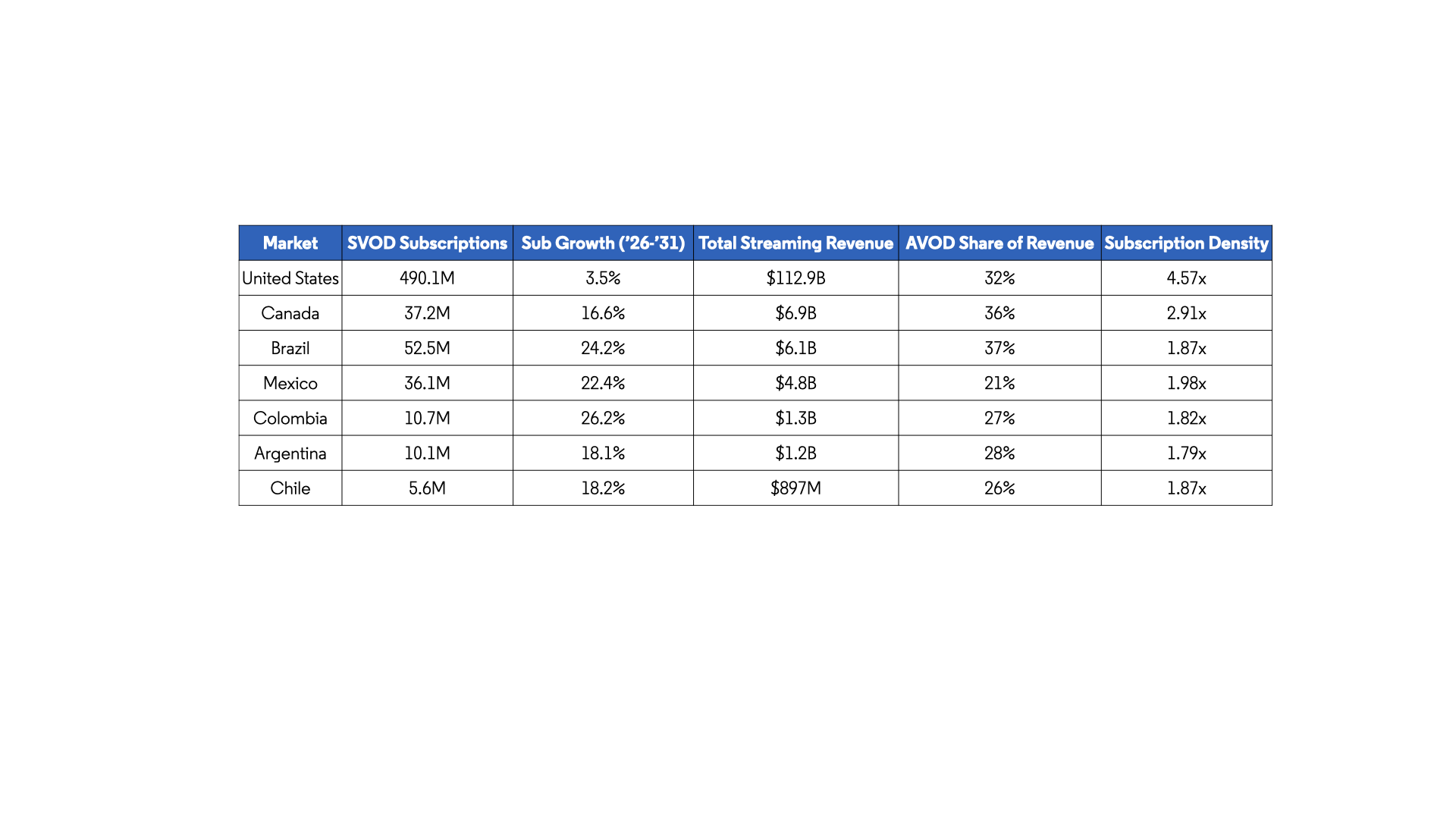

In North America, the subscriber base is effectively saturated. US SVOD subscriptions grow just 3.5% over five years - from 490M to 507M - while paying subscribers barely move, from 107M to 109M. Growth is coming almost entirely from subscription stacking: consumers adding second, third and fourth services rather than new households entering the market. The question has shifted from "how do we acquire subscribers?" to "how do we get more from the ones we have?"

Latin America is still answering the first question. SVOD subscriptions grow 25% to 178M by 2031. Colombia expands 26%, Brazil 24%, Mexico 23%. Broadband rollout is actively opening up new households - Colombia alone adds 1.6 million fixed broadband lines over the forecast period. This is real growth, not repackaged growth.

What does that mean for operators and investors? A two-speed Americas market. North America rewards revenue-per-subscriber growth through hybrid models. Latin America rewards positioning to capture households that are still coming online for the first time.

North America: Consolidation, Hybrid Tiers and the End of the Second Tier

The defining feature of the North American market in 2026 isn't growth. It's reorganisation.

The pending Paramount–Warner Bros. Discovery merger - a $31/share deal expected to close in Q3 2026 - will combine Max and Paramount+ into a single platform. At 200M+ combined global subscribers, the merged entity will have the scale to compete directly with Netflix and Disney. For the rest of the pack, the implications are stark. Peacock, Apple TV+ and any remaining mid-tier service now face a market where the top three platforms control an even larger share of attention, content spend and pricing power.

Comcast's spin-off of its cable networks into Versant Media Group, completed in January 2026, underscores the split. Legacy distribution is being carved off. Streaming is the business now.

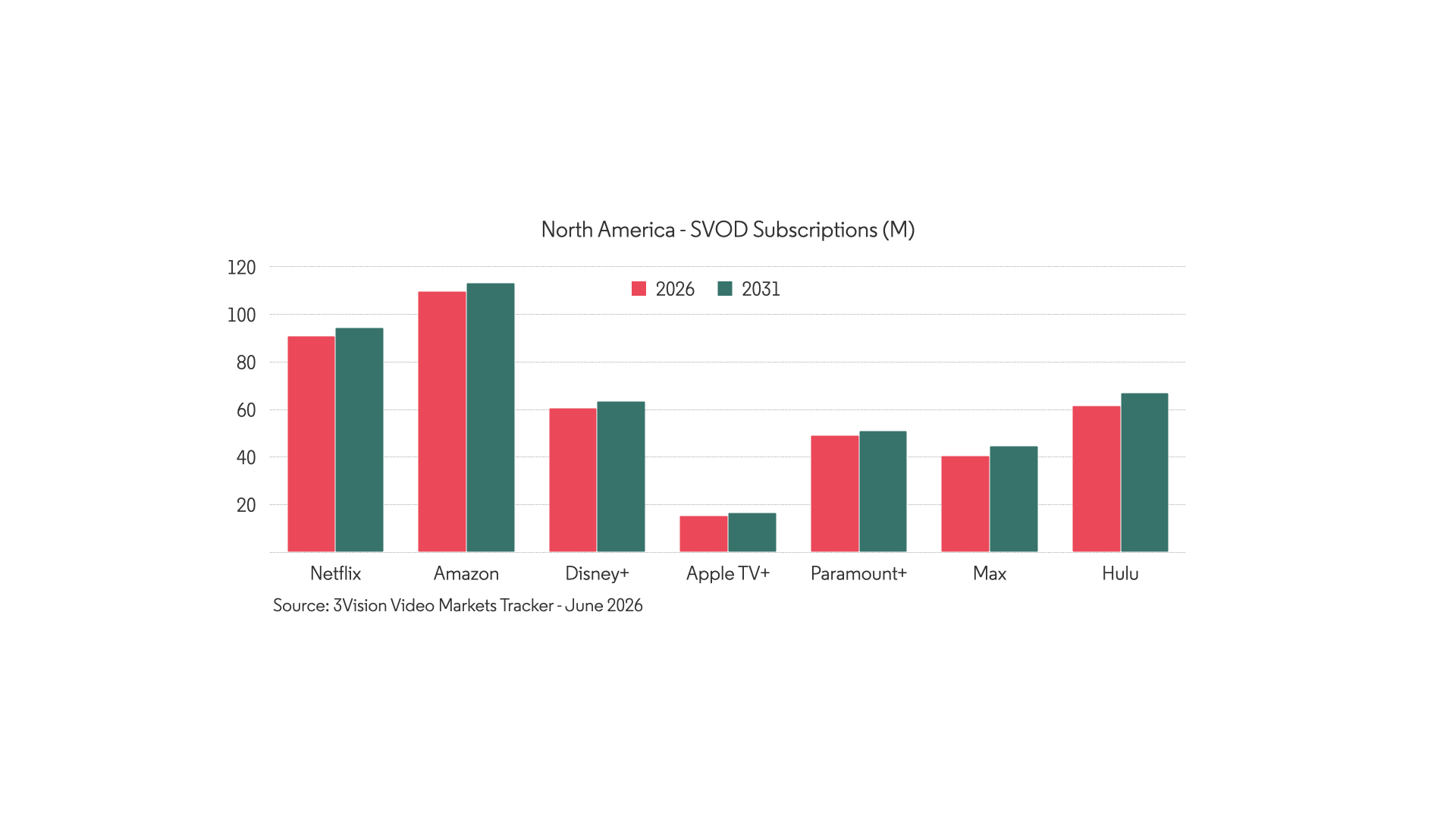

Amazon Prime Video and Netflix remain co-leaders in the US, both holding above 80M subscriptions through 2031. Amazon's launch of Prime Video Ultra in April 2026 - a premium ad-free tier at $4.99/month — signals a new phase of tier stratification: designed to monetise a massive installed base rather than grow it. Disney+ holds at 57M US subscriptions, anchored by the Disney+/Hulu/ESPN Unlimited bundle at $29.99/month - arguably the most integrated sports-entertainment-streaming proposition in the market.

Hybrid subscriptions tell the monetisation story most clearly. Ad-supported tiers rise from 70M to 90M across North America. The hybrid model isn't an experiment any more. Every major platform raised prices $1–$3 between January 2025 and January 2026. Pricing power is strengthening. The ad tier keeps price-sensitive subscribers on board while premium pricing pushes higher.

In Canada, the market follows a similar trajectory at smaller scale. SVOD subscriptions grow from 37M to 43M, with Netflix, Amazon Prime Video and Disney+ leading, and domestic players Crave and StackTV holding important positions. Canadian AVOD grows 71% to $4.2B by 2031 - faster than SVOD - confirming the ad-led growth story isn't a US-only phenomenon.

Across North America, revenue growth is now decoupling from subscriber growth. The competitive advantage belongs to platforms that can layer subscription fees, ad-supported tiers and bundled propositions against the same household.

Sports Streaming Rights: The Arms Race Reshaping Retention

Live sports have become the single most important competitive lever in North American streaming. And the investment is accelerating.

Amazon's NBA deal is now active: 66 regular-season games, the Emirates NBA Cup and Conference Finals, layered on top of its existing Thursday Night Football package. Netflix has expanded to a five-game NFL package for 2026–27. Apple TV+ holds exclusive US Formula 1 rights from 2026. WWE moved to Netflix and ESPN Unlimited. NBC brought the NBA back to Peacock with an exclusive NFL playoff window. YouTube is in advanced negotiations for a multi-game NFL streaming package.

The scale of this shift has drawn regulatory attention. The DOJ is now investigating whether the NFL's expanding web of exclusive streaming deals raises antitrust concerns under the Sports Broadcasting Act.

ESPN Unlimited's standalone launch in August 2025 - at $29.99/month, bundled with Disney+ and Hulu - marks ESPN's first direct entry into the streaming subscription market. It signals that sports rights holders increasingly see DTC distribution as the primary revenue channel, not a secondary one.

In Latin America, the FIFA World Cup 2026 plays a parallel role. Co-hosted across the US, Canada and Mexico, the tournament gives platforms across the region a near-term engagement boost. In Mexico, ViX serves as a key broadcaster alongside Televisa and TV Azteca. In Argentina and Colombia, Disney+ carries ESPN's exclusive coverage. Paramount+ benefits from DSPORTS coverage and its newly secured UEFA Champions League rights for 2027–2031.

Sports aren't just a North American story - they're becoming a hemisphere-wide streaming driver. For anyone evaluating platform valuations, the presence of a live sports rights portfolio is fast becoming a proxy for subscriber stickiness. Platforms without sports face higher churn.

Latin America: Where the Subscribers Still Are

If North America's story is consolidation, Latin America's is construction.

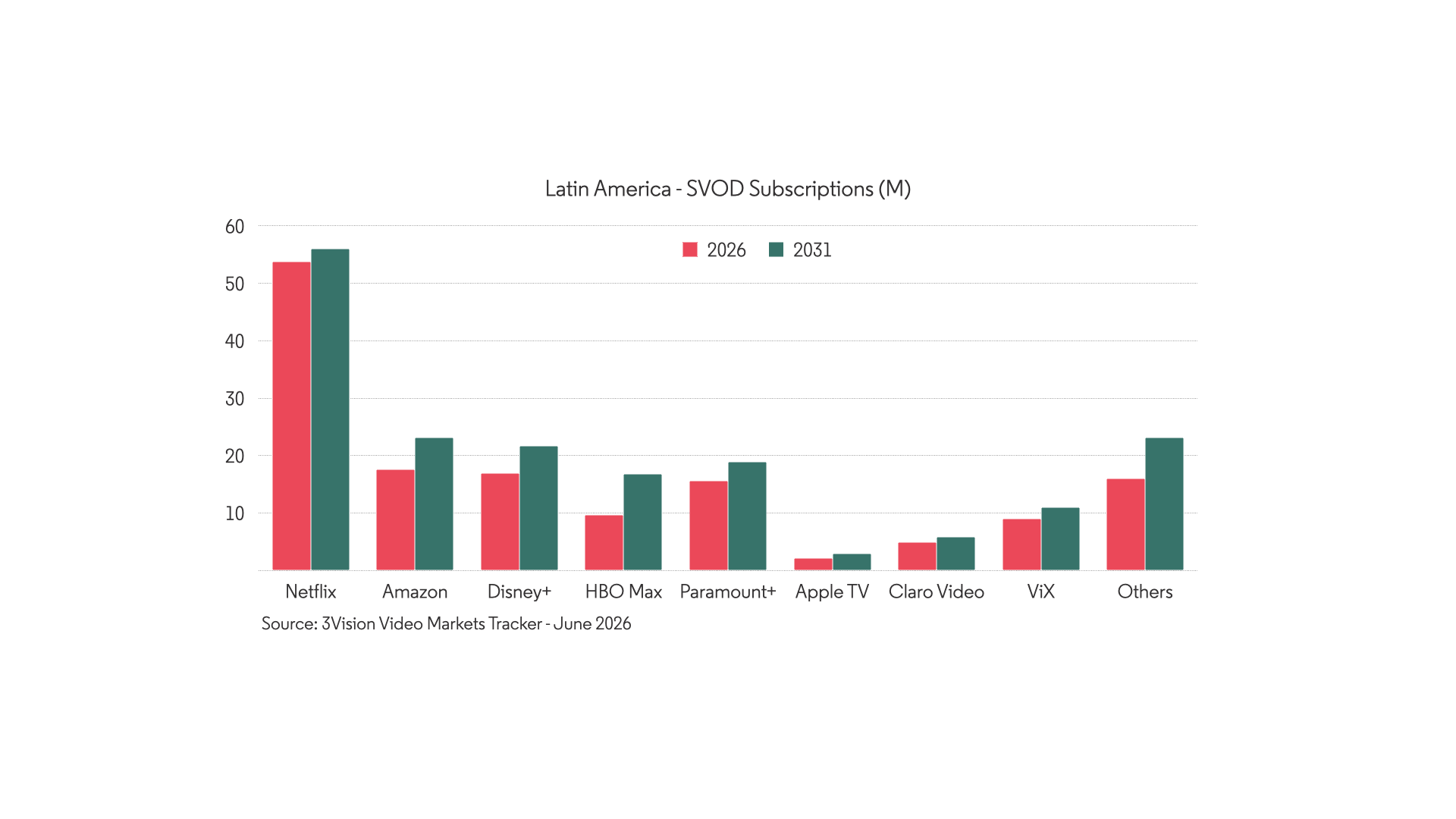

Netflix dominates at 53.8M subscriptions, growing to 56.1M by 2031. But the more interesting dynamics sit further down the stack. Amazon Prime Video grows from 17.5M to 23.1M. Disney+ - which absorbed Star+ in mid-2024, folding its content and ESPN into a unified LatAm offering - expands from 16.9M to 21.7M. Max more than doubles from 9.6M to 16.8M, making it comfortably the fastest-growing global platform in the region. The pending Paramount-WBD merger will reshape this competitive layer just as dramatically as in North America.

Mexico - the region's second-largest market at 36.1M subscriptions - already has the highest stacking density in Latin America at 1.98 subscriptions per subscriber, rising to 2.22 by 2031. Amazon Prime Video is the fastest-growing major platform there in absolute terms, adding 2.5M subscriptions over the forecast. And as a World Cup co-host, Mexico enters the forecast period with a significant boost across multiple platforms.

ViX deserves particular attention. At 9M subscriptions growing to 11M by 2031, it's the fastest-growing major streamer in the Americas - fuelled by its freemium model, retail bundling with OXXO and Mercado Libre, a Disney+ bundle, and Spanish-language content including microdramas. In the US, ViX grows from 4.8M to 6.6M, reflecting the expanding Hispanic streaming audience. It's one of the few platforms with a credible cross-border growth story spanning both halves of the hemisphere.

Country-level dynamics vary meaningfully. Colombia is the fastest-growing market at 26% subscription growth, driven by broadband expansion from 9.8M to 11.4M fixed lines. Max doubles from 0.88M to 1.49M there, and the "Others" category nearly triples - suggesting real headroom for platform diversification. Chile, by contrast, is approaching saturation: Netflix already reaches over 40% of TV households. Chile's next phase is about monetising depth, not chasing reach.

Pricing remains a real constraint as subscription growth continues to outpace revenue growth. SVOD subscriptions rise 25% while SVOD revenues grow 14%. Per-subscriber monetisation still has room to develop. For content owners, that gap compresses per-title economics and puts a premium on Spanish-language originals with pan-regional appeal.

Brazil: The Region's Outlier

Brazil is the largest market in Latin America by both subscriptions (52.5M) and revenue ($6.1B). And it operates differently from every other country in the region.

The difference is Globoplay. At 11.8M subscriptions growing to 14.7M by 2031, Globoplay isn't just a streaming platform - it's the digital extension of Grupo Globo's legacy advertising relationships. The platform reached profitability for the first time in late 2025 after a decade of losses, with 30% subscriber growth and 4.5 billion hours watched. Globoplay alone generates $640M in AVOD and $166M in FAST revenue. Together with YouTube ($1.06B), it accounts for 75% of Brazil's AVOD market.

That gives Brazil a very different revenue profile. AVOD already represents 37% of total streaming revenue - far higher than any other market in the region - and the gap will widen. Disney's closure of six linear channels in Brazil in February 2025 (including Disney Channel, FX and National Geographic) accelerates the DTC shift.

Brazil isn't transitioning from linear to streaming. It's already there. Globoplay's path to profitability offers a replicable model for other Latin American broadcasters, and the maturity of Brazil's ad-supported ecosystem makes it the region's most developed streaming advertising market.

AVOD and FAST Revenue: The Advertising Opportunity

Across both regions, ad-supported streaming is the fastest-growing revenue segment.

In North America, AVOD grows 32% to $50.3B, with FAST reaching $5.6B (+41%). In Latin America, AVOD grows 74% to $8.0B, with FAST more than doubling from $1.0B to $2.1B. In Mexico, ViX's FAST channels alone generate $219M - the single largest FAST contributor in the country. Streaming advertising across Latin America is projected to double over the next five years.

The shift to hybrid monetisation is now embedded. In North America, 90M hybrid subscriptions by 2031. In Latin America, a rapidly expanding AVOD infrastructure built on top of local platforms with deep advertising relationships. The Americas aren't choosing between subscription and advertising. They're building both at the same time. And the platforms that can do both at scale will define the next five years.

For investors, advertising revenue is no longer a supplementary line item - it's a co-primary revenue engine. The rapid growth of FAST channels also raises important questions about how it interacts with legacy linear TV ad markets.

All data in this forecast comes from our Video Markets Tracker, which covers SVOD subscriber, streaming revenue, AVOD, FAST, TVOD and EST forecasts across North America, Latin America and five other global regions — with platform-level and country-level detail to 2031. Want the full dataset, competitive benchmarking, or a walkthrough? Get in touch.

.svg)