HBO Max launches in the UK on 26 March, following recent rollouts in Germany and Italy. As the platform continues its EMEA expansion, its approach to third-party acquisitions deserves close attention.

Warner Bros. Discovery’s vertical integration means HBO Max has a substantial in-house pipeline. But history shows that launch periods often create distinct acquisition windows for scripted series. Show Tracker data from previous launches highlights a clear pattern.

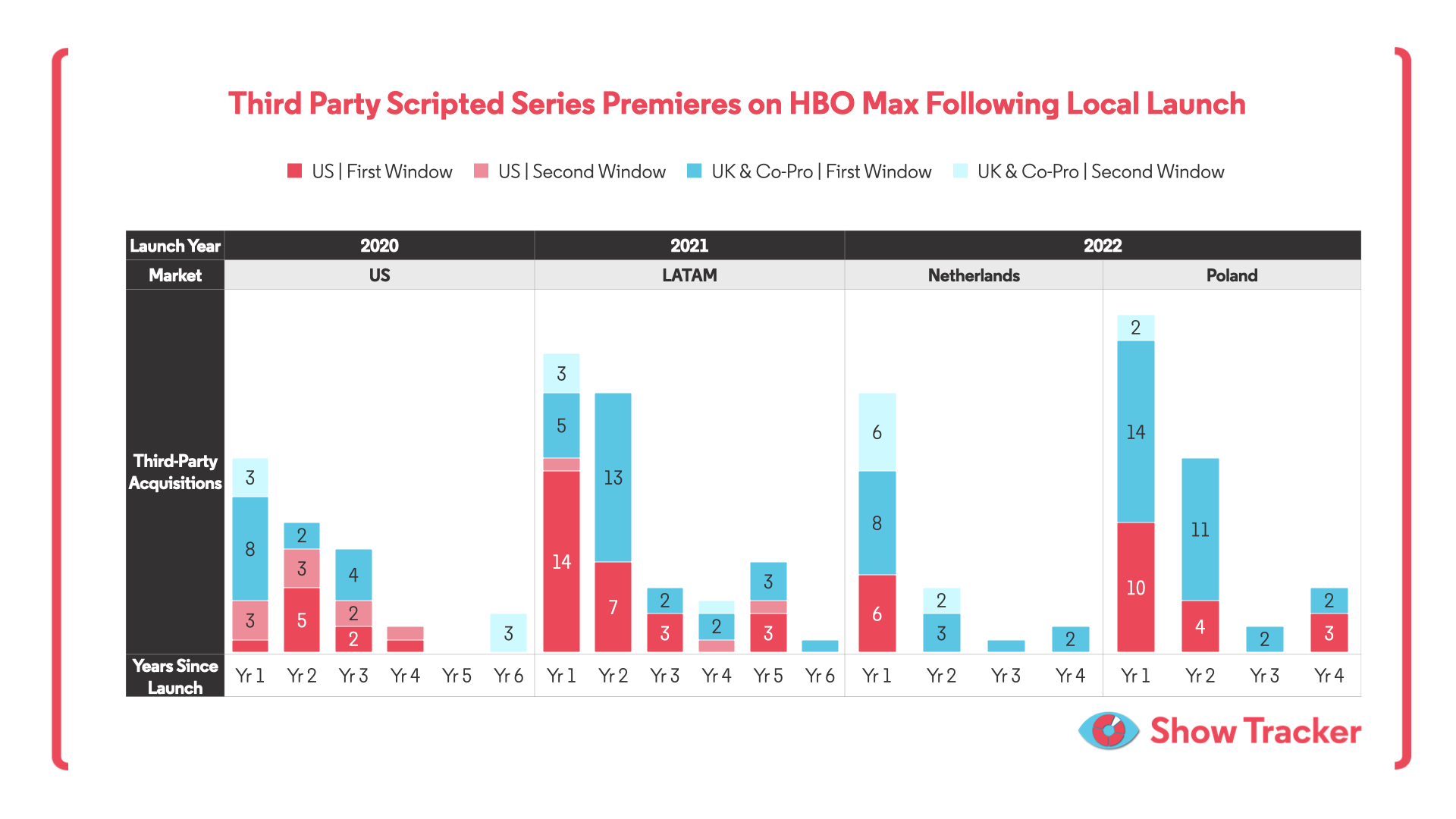

When HBO Max debuted in the US in 2020, it did so in extraordinary circumstances. The pandemic disrupted production pipelines and accelerated streaming demand. During this period, the service acquired a significant volume of UK titles. Several co-commissions were also agreed in the early years. Acquisition levels were notably higher in year one than in subsequent years.

A similar trajectory can be seen in LATAM, the Netherlands and Poland. LATAM leaned heavily into US first-window titles in its first year. Poland recorded the highest volume of first-year acquisitions of any HBO Max launch market during its debut in 2022. In each of these cases, activity tapered after launch.

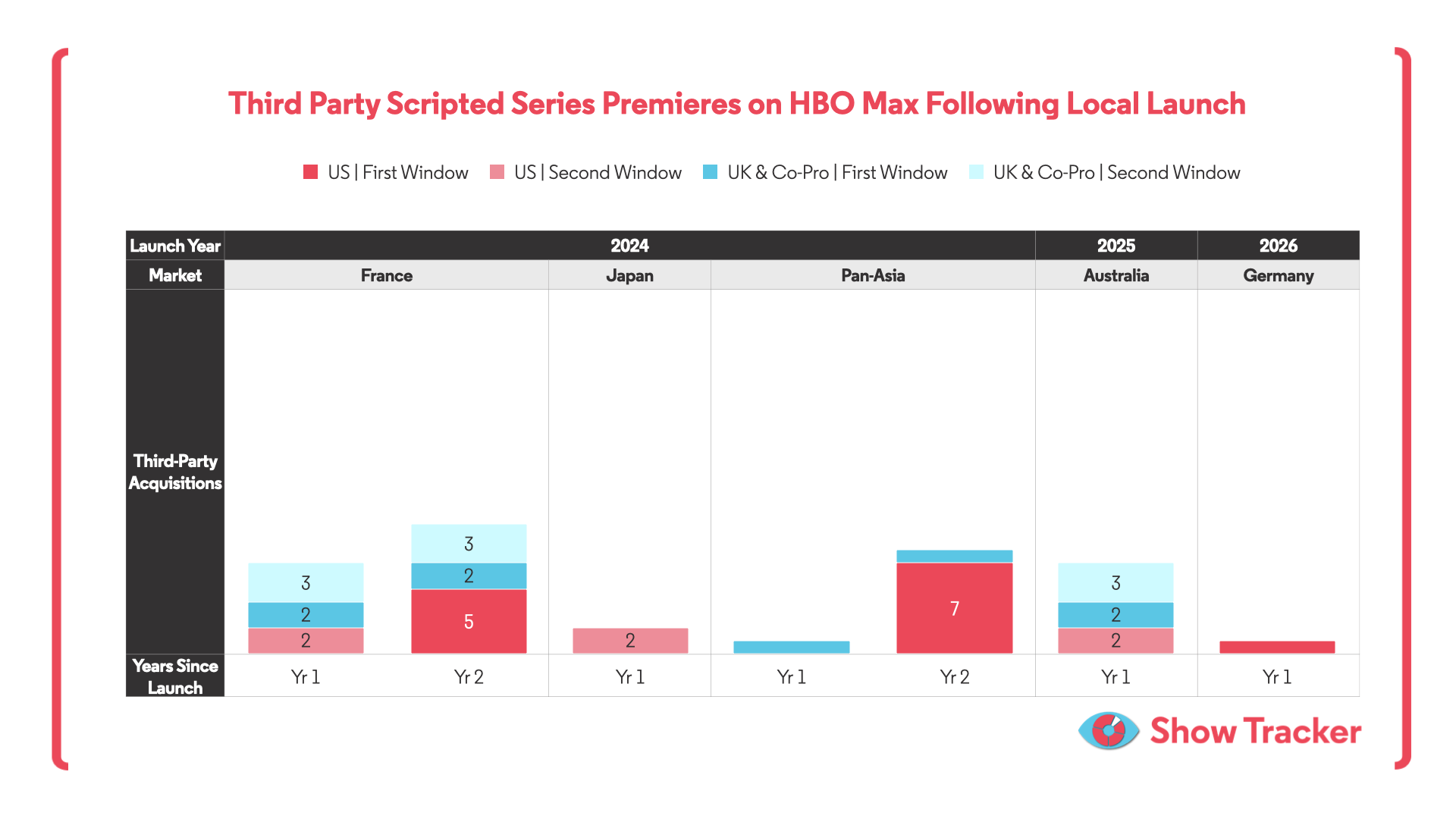

The implication was straightforward: HBO Max supplemented its vertically integrated slate aggressively at launch, then reduced reliance on third-party supply as its pipeline matured. But more recent launches suggest a possible refinement of that model. France and Pan-Asia both instead saw increased acquisition activity in year two rather than an immediate drop-off.

These are not large volumes of acquisitions considering the level of Warner titles coming to service day-and-date with the US, but they do indicate some level of ongoing interest in third-party titles rather than complete withdrawal from the market post-launch.

The UK presents a different environment. UK scripted content will already have established a first window home with its commissioner, and the market is one of the highest for US distribution thanks to vertical integration and reliable local buyers like Sky. This limits the scale of first window acquisitions HBO Max can make in the UK. As a result, the more realistic opportunity for distributors is likely to lie in second windows.

The UK may also be a particularly interesting market for HBO Max because of Sky’s central position. Sky has long-standing output deals with Warner/HBO and Disney. These relationships are now developing into deeper bundling arrangements, where streaming services are included as part of Sky’s core offer. At the same time, Sky continues to work closely with other studios including its owner, NBCUniversal. How these relationships work together in practice, and how prominently HBO Max is positioned within Sky’s offer, will make the UK a fascinating market to follow.

Tracking HBO Max’s launches around the world and using them as an opportunity to sell content, while monitoring sudden spikes on the local level, will become increasingly critical for third-party distributors looking for a well-funded buyer of their titles.

.svg)