Introduction

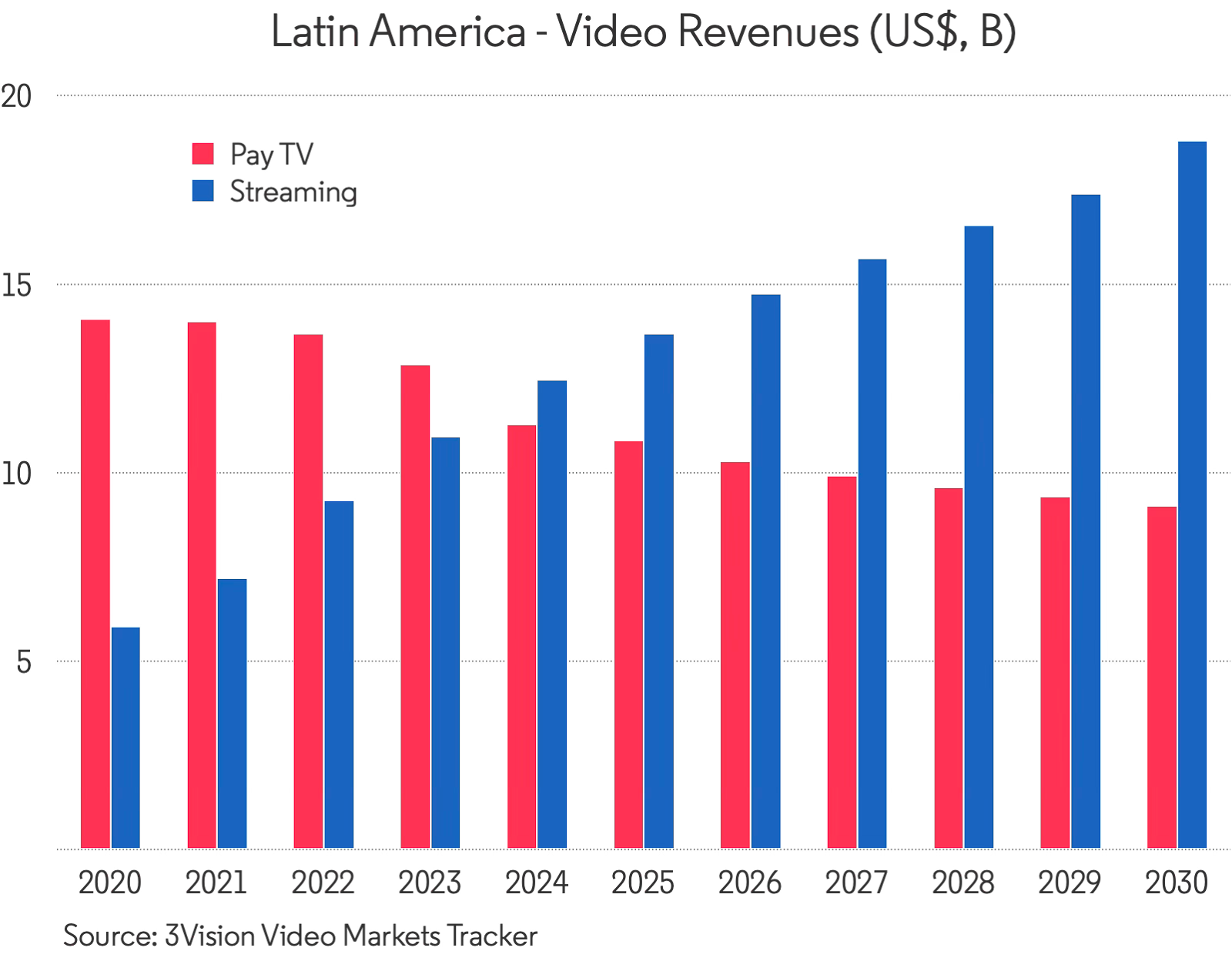

The Latin America video market — worth over $24bn in combined Pay TV and Streaming revenues by 2030 — is no longer defined by the shift from Pay TV to Streaming. That transition has already taken place. The more important story now is how Streaming is growing and why its growth looks very different from the early adoption phase.

OTT Revenue Growth and Streaming Market Trends in Latin America

Streaming platforms are firmly in growth mode, but not primarily by adding new households. Total OTT revenues rise from approximately $11bn in 2023 to almost $19bn by 2030, overtaking Pay TV and becoming the region’s dominant video revenue pool. Yet the number of households paying for at least one SVOD service grows more modestly, from around 66 million to about 84 million over the period.

SVOD Growth and Subscription Density in Latin America

The real expansion happens inside the home. Total SVOD subscriptions climb from roughly 111 million in 2023 to around 176 million by 2030, pushing average subscriptions per paying household from 1.68 to just over 2.0. Latin America is moving from a market defined by penetration to one defined by density, as consumers layer services rather than continuously adding new ones.

AVOD and FAST Growth in Latin America’s Video Market

At the same time, advertising has become the critical release valve for price sensitivity. AVOD revenues are set to almost triple, rising from just over $2bn in 2023 to around $6bn by 2030, accounting for almost half of all incremental video on demand (VOD) revenue growth. FAST is the standout within this segment, scaling from under $400 million to around $1.6bn, and growing from a niche format into a meaningful component of the regional connected TV (CTV) advertising market.

Streaming Platform Strategies in Latin America (Disney+, Netflix, Max, Paramount+)

We can see this in recent events. Disney moved to simplify its regional offering by folding Star+ directly into Disney+ in 2024, a signal that bundling, tiering and monetisation efficiency now outweigh rapid service proliferation. Likewise, Netflix has already repositioned growth in Latin America around its ad-supported tier; while Max and Paramount+ have both framed Latin America (LATAM) as a priority market for hybrid models, using ad-supported tiers and telco distribution to balance affordability with scale.

The Role of Advertising and Subscription Stacking in Streaming Growth

These two trends - stacking and advertising - are closely linked. As households subscribe to more services, pressure on discretionary spend increases. Hybrid ad-supported tiers and FAST channels allow platforms to expand reach and usage without relying solely on higher subscription prices, while advertisers gain access to TV-like audiences at scale.

Pay TV Decline in Latin America

By contrast, traditional Pay TV continues its long, gradual decline. Regional Pay TV revenues fall from around $13bn in 2023 to roughly $9bn by 2030, while subscriber numbers edge down only slightly, from about 55 million to just over 52 million. This stability masks a deeper issue: ARPU pressure, prepaid offers and multi-play bundling are steadily reducing the ability of local operators to generate incremental value.

Future of the Latin America Video Market

The next phase of Latin America's OTT market will not be won by who signs up the most households. It will be shaped by who can monetise denser households most effectively, balancing subscriptions, hybrid tiers and FAST to unlock sustainable growth in a post-Pay-TV world.

Conclusion: A Market Defined by Density, Not Discovery

- Subscription Stacking: Total SVOD subscriptions climb from roughly 111 million in 2023 to around 176 million by 2030, with average subscriptions per paying household rising from 1.68 to just over 2.0

- Advertising Growth: AVOD revenues almost triple, rising from just over $2bn in 2023 to around $6bn by 2030, with FAST scaling from under $400 million to around $1.6bn

- Pay TV Decline: Pay TV revenues fall from around $13bn in 2023 to roughly $9bn by 2030, while subscriber numbers decline only modestly from about 55 million to just over 52 million

- Platform Strategy: Disney, Netflix, Max and Paramount+ are all prioritising hybrid ad-supported tiers and bundling to balance affordability with scale across the region

Explore the Video Markets Tracker – detailed forecasts and insights on Global Video Market, including Streaming, Pay TV, SVOD, AVOD, and FAST adoption

.svg)