Sub-Saharan Africa Video Market Forecast to 2030:

- Streaming Revenue: $2.2B

- Pay TV Revenue: $5.9B

- SVOD Subscribers: 10.7M

- Pay TV Subscribers: 56.4M

- Streaming Market Share: 27%

The latest data from 3Vision's Video Markets Tracker shows that the Sub-Saharan Africa video market is not following the global pattern of cord-cutting. In more mature regions, Streaming has largely displaced Pay TV as the primary growth engine of the TV industry. In Sub-Saharan Africa, however, the picture is fundamentally different. The market is expanding across multiple layers, with both Pay TV and Streaming growing in parallel rather than competing in a zero-sum shift.

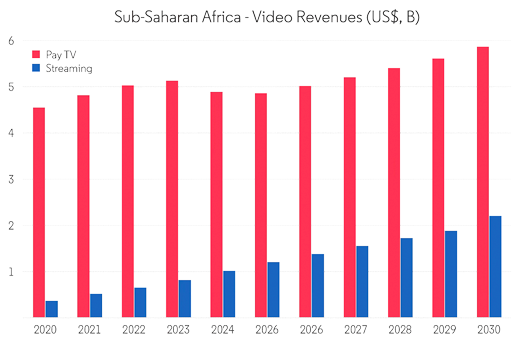

This dynamic is clearly reflected in long-term revenue trends. Streaming revenues grow from $372.4M in 2020 to $2.2B by 2030, marking a near sixfold increase over the decade. Over the same period, Pay TV revenues expand from $4.6B to $5.9B, reinforcing its continued dominance in absolute terms. While Streaming is scaling rapidly, it is doing so from a much smaller base, and the structural role of Pay TV remains firmly intact.

By 2030, this results in a video market that looks very different to those in North America or Western Europe. Rather than a transition from one model to another, Sub-Saharan Africa is characterised by a layered ecosystem in which both traditional and digital models coexist, serving different needs and price points.

Sub-Saharan Africa Video Market Structure: Rebalancing, Not Replacement

One of the clearest indicators of this structural difference is the evolving share of total video revenues. In 2026, Streaming accounts for 22% of the total video market, with Pay TV representing 78%. By 2030, Streaming’s share rises to 27%, while Pay TV declines modestly to 73%.

This shift highlights two important points. First, Streaming is undeniably gaining ground and becoming a meaningful part of the overall market. Second, and more importantly, Pay TV is not being displaced. Instead, both segments continue to grow in absolute terms, with Streaming gradually increasing its share without triggering a collapse in Pay TV revenues.

This contrasts sharply with more mature markets, where Streaming growth has come largely at the expense of Pay TV subscriptions and revenues. In Sub-Saharan Africa, the expansion of Streaming is additive rather than substitutive.

Streaming Growth in Sub-Saharan Africa: Mobile-First Expansion Across SVOD and AVOD

Streaming growth in Sub-Saharan Africa is being driven by a combination of structural and technological factors. Chief among these is the rapid rise in smartphone penetration, which has fundamentally changed how audiences access video content. For many consumers, particularly in lower-income segments, mobile devices represent the primary—and often only—gateway to OTT Streaming services.

As a result, the region has seen the emergence of mobile-first pricing models and lower-cost service tiers, making Streaming more accessible to a broader audience. This has been a key driver of adoption across major markets such as Nigeria, South Africa and Kenya.

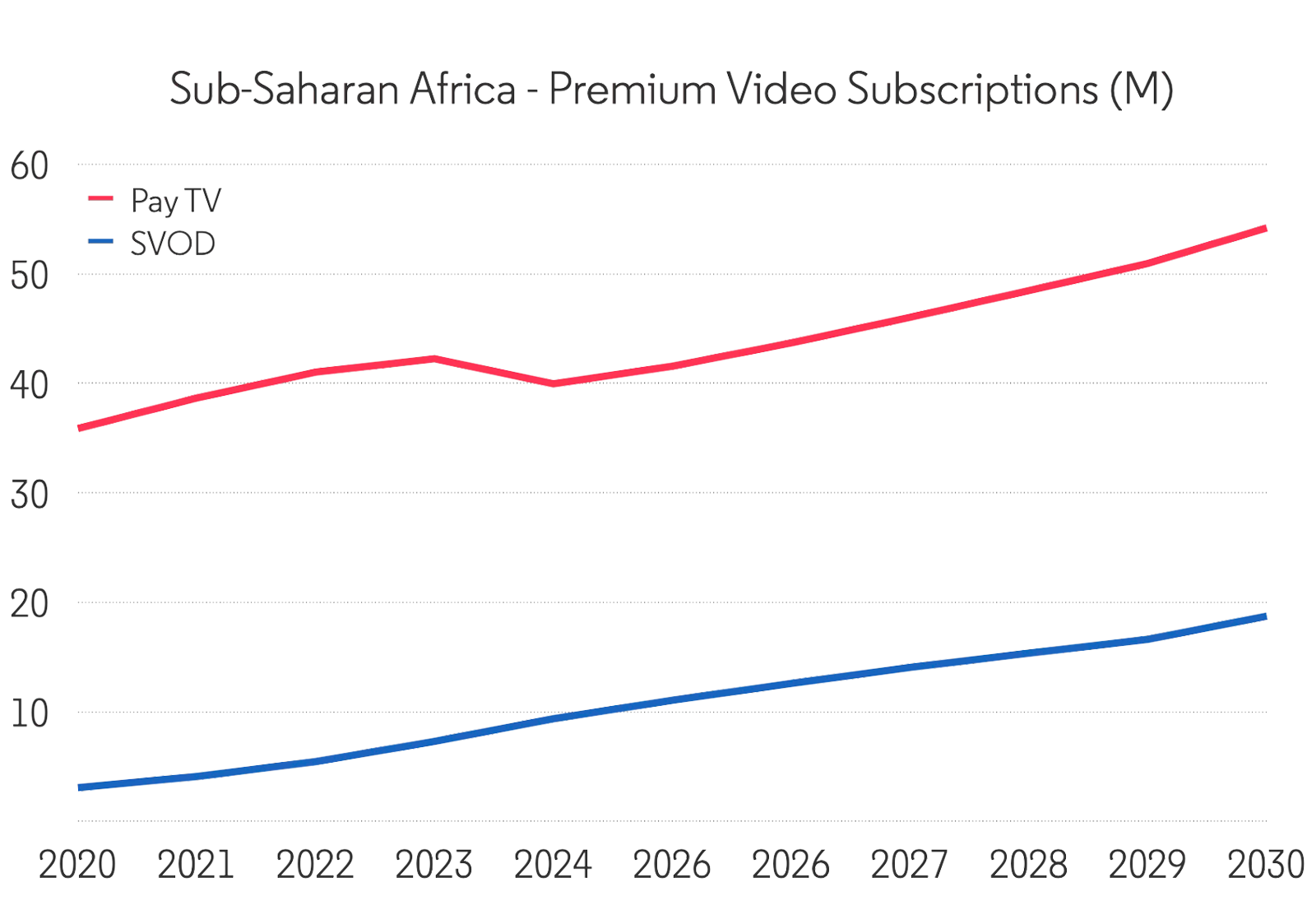

Within Streaming, both subscription and advertising-supported models are expanding, albeit at different speeds. According to 3Vision's Video Markets Tracker, SVOD remains the largest component, with subscribers increasing from 7.8M in 2026 to 10.7M by 2030. However, total subscriptions reach 18.7M over the same period, reflecting increased stacking as users combine multiple services. By 2030, the average user subscribes to 1.75 services, signalling a gradual maturation of the market.

At the same time, AVOD is growing even faster, supported by the development of digital advertising ecosystems across the region. 3Vision's Video Markets Tracker forecasts AVOD revenues reaching $330M by 2030, as advertisers increasingly shift budgets towards digital video on demand (VOD) platforms.

FAST, while still relatively small, is also beginning to emerge as a distinct segment. Revenues grow from $7.4M in 2026 to $18.7M by 2030, indicating early-stage momentum. Although FAST remains a minor contributor in absolute terms, its growth trajectory suggests it could become a more significant part of the ecosystem over time, particularly as connected TV (CTV) adoption increases..

Monetisation Constraints: Growth in Scale, Not Yet in ARPU

Despite strong growth in users and revenues, Streaming monetisation in Sub-Saharan Africa remains constrained. SVOD monthly ARPU increases only modestly, from $7.21 in 2026 to $7.59 by 2030, reflecting the continued importance of affordability in shaping pricing strategies.

This relatively low ARPU level is a direct consequence of the region’s economic profile, where disposable incomes are lower and price sensitivity is high. Payment infrastructure also remains fragmented, with limited access to credit cards and reliance on alternative payment methods such as mobile money.

As a result, Streaming growth is driven primarily by user acquisition rather than revenue per user. Platforms are focused on expanding their reach and building scale, often at the expense of near-term monetisation.

Pay TV in Sub-Saharan Africa: Resilience and Structural Importance

While Streaming is expanding rapidly, Pay TV continues to play a central role in the Sub-Saharan Africa video market. According to 3Vision's Video Markets Tracker, subscriber numbers grow from 45.6M in 2026 to 56.4M by 2030, with penetration stabilising at approximately 41% of TV households.

This resilience is underpinned by several factors. First, Pay TV platforms benefit from established distribution networks, particularly in markets where broadband infrastructure remains underdeveloped. Satellite and terrestrial delivery methods provide reliable access to content in areas where internet connectivity is limited or inconsistent.

Second, Pay TV continues to hold a strong position in premium content, particularly sports. Live sports rights remain a key driver of subscriptions, offering content that is difficult to replicate in a purely on-demand Streaming environment.

Third, bundled offerings and tiered pricing structures allow Pay TV operators to cater to a wide range of consumer segments, from entry-level packages to premium tiers.

The recovery following the shutdown of StarSat in 2024 further underscores the structural importance of Pay TV. While the closure created a temporary dip in subscriber numbers, the market has since stabilised and resumed growth, with subscribers redistributed across other platforms.

Pay TV Monetisation: Higher ARPU, Slower Growth

In contrast to Streaming, Pay TV monetisation is stronger but growth is more constrained. Monthly ARPU declines slightly from $9.18 in 2026 to $8.68 by 2030, reflecting increasing pricing pressure and the need to maintain affordability.

Unlike Streaming, where growth is driven by new users, Pay TV is approaching a more mature phase in many markets. Subscriber growth continues, but at a slower pace, and revenue expansion is increasingly dependent on pricing strategies rather than scale.

This creates a clear divergence between the two models. Pay TV generates higher revenue per user but has limited room for expansion, while Streaming has greater growth potential but lower monetisation levels.

Country-Level Dynamics: Nigeria, South Africa and Kenya

The overall trends in the Sub-Saharan Africa video market are shaped by significant variation at the country level, with key markets driving much of the growth.

In Nigeria, Streaming adoption is accelerating rapidly. SVOD subscriptions grow from 2.4M in 2026 to 3.7M by 2030, reflecting the country’s large population and increasing digital connectivity. At the same time, Pay TV remains highly relevant, with subscriber numbers exceeding 10M by the end of the decade.

South Africa represents a more mature market, with higher levels of both Pay TV penetration and Streaming adoption. SVOD penetration increases from 32% of TV households in 2026 to 40% by 2030, indicating a steady shift towards digital services. However, Pay TV remains deeply entrenched, supported by strong incumbents and premium content offerings.

Kenya, meanwhile, highlights the role of mobile-first growth. Between 2026 and 2030, SVOD subscriptions increase by 58%, while Streaming revenues grow by 70%, underscoring the rapid expansion of digital video consumption. The market is characterised by strong adoption of mobile video and mobile-based services, with increasing integration of mobile payments

Key Platforms: Global and Regional Players Compete

The competitive landscape in Sub-Saharan Africa reflects a mix of global Streaming platforms and regional Pay TV operators. International services such as Netflix and Amazon Prime Video are expanding their presence, leveraging global content libraries and increasing investment in local programming.

At the same time, regional players such as MultiChoice, through platforms like DStv and (until the recent shutdown) Showmax, continue to play a dominant role. These operators benefit from deep local market knowledge, established distribution networks and strong content portfolios, particularly in sports and local programming.

This creates a hybrid competitive environment in which global and local players coexist, each targeting different segments of the market.

Why Sub-Saharan Africa Is Different: Structural Drivers of a Layered Market

The coexistence of Pay TV and Streaming in Sub-Saharan Africa is not accidental. It is the result of a set of structural factors that differentiate the region from more mature markets.

Affordability remains a key constraint, limiting the ability of consumers to adopt multiple high-cost services. This creates space for both lower-cost Streaming options and tiered Pay TV offerings.

Infrastructure also plays a critical role. While connectivity is improving, it remains uneven across the region, making traditional broadcast and satellite delivery methods more reliable in many areas.

Finally, payment systems continue to shape consumption patterns. The prevalence of mobile money and prepaid models favours flexible, low-commitment services, influencing both Streaming and Pay TV pricing strategies.

Streaming vs Pay TV in Sub-Saharan Africa: A Complementary Relationship

Taken together, these factors result in a video market where Streaming and Pay TV are complementary rather than directly competitive. Each model serves different consumer needs, operates at different price points and relies on different distribution mechanisms.

Streaming provides flexibility, accessibility and lower-cost entry points, particularly for younger and more digitally engaged audiences. Pay TV, by contrast, offers reliability, premium content and bundled value, appealing to households seeking a more traditional viewing experience.

The overlap between the two remains limited, although it is likely to increase over time as markets continue to develop.

Sub-Saharan Africa Video Market Outlook to 2030

Looking ahead, the Sub-Saharan Africa video streaming market is set to continue expanding across both Pay TV and Streaming. Streaming will grow faster and increase its share of the market, but Pay TV will remain the dominant revenue pool.

The absence of fully developed hybrid SVOD models suggests that the next phase of evolution is still to come. As platforms experiment with pricing, bundling and advertising-supported models, the balance between subscription and advertising revenues is likely to shift further.

For now, however, the defining characteristic of the market is its layered structure. Growth is not driven by replacement, but by expansion across multiple models, each addressing different segments of a diverse and rapidly evolving audience base.

Conclusion: A Market Defined by Expansion, Not Disruption

Sub-Saharan Africa stands apart from global video market trends. Rather than following a linear path from Pay TV to Streaming, the region is building a more complex and layered ecosystem in which both models coexist and grow.

Streaming is scaling rapidly, driven by mobile-first adoption and increasing accessibility. Pay TV remains resilient, supported by strong content and established infrastructure. Together, they form a market that is defined less by disruption and more by opportunity.

For operators, platforms and investors, this presents a clear strategic imperative: success in Sub-Saharan Africa will depend not on choosing between Pay TV and Streaming, but on understanding how the two can evolve together within a highly fragmented, price-sensitive and still underpenetrated market.

Conclusion: A Market Defined by Expansion, Not Disruption

- Layered Market: Sub-Saharan Africa is not following the linear path from Pay TV to Streaming; both models coexist and grow.

- Streaming Growth: Mobile-first adoption and increasing accessibility are driving rapid Streaming expansion.

- Pay TV Resilience: Supported by strong content and established infrastructure, Pay TV remains the dominant revenue pool.

- Complementary Models: Success depends on understanding how Streaming and Pay TV can evolve together.

- Opportunity Over Disruption: Growth is additive, with multiple models expanding in a fragmented, price-sensitive, underpenetrated market.

Explore 3Vision's Video Markets Tracker – detailed forecasts and insights on Global Video Market, including Streaming, Pay TV, SVOD, AVOD, and FAST adoption

.svg)