MENA Streaming Market 2025–2030: OTT Revenue, SVOD Growth and Satellite Decline

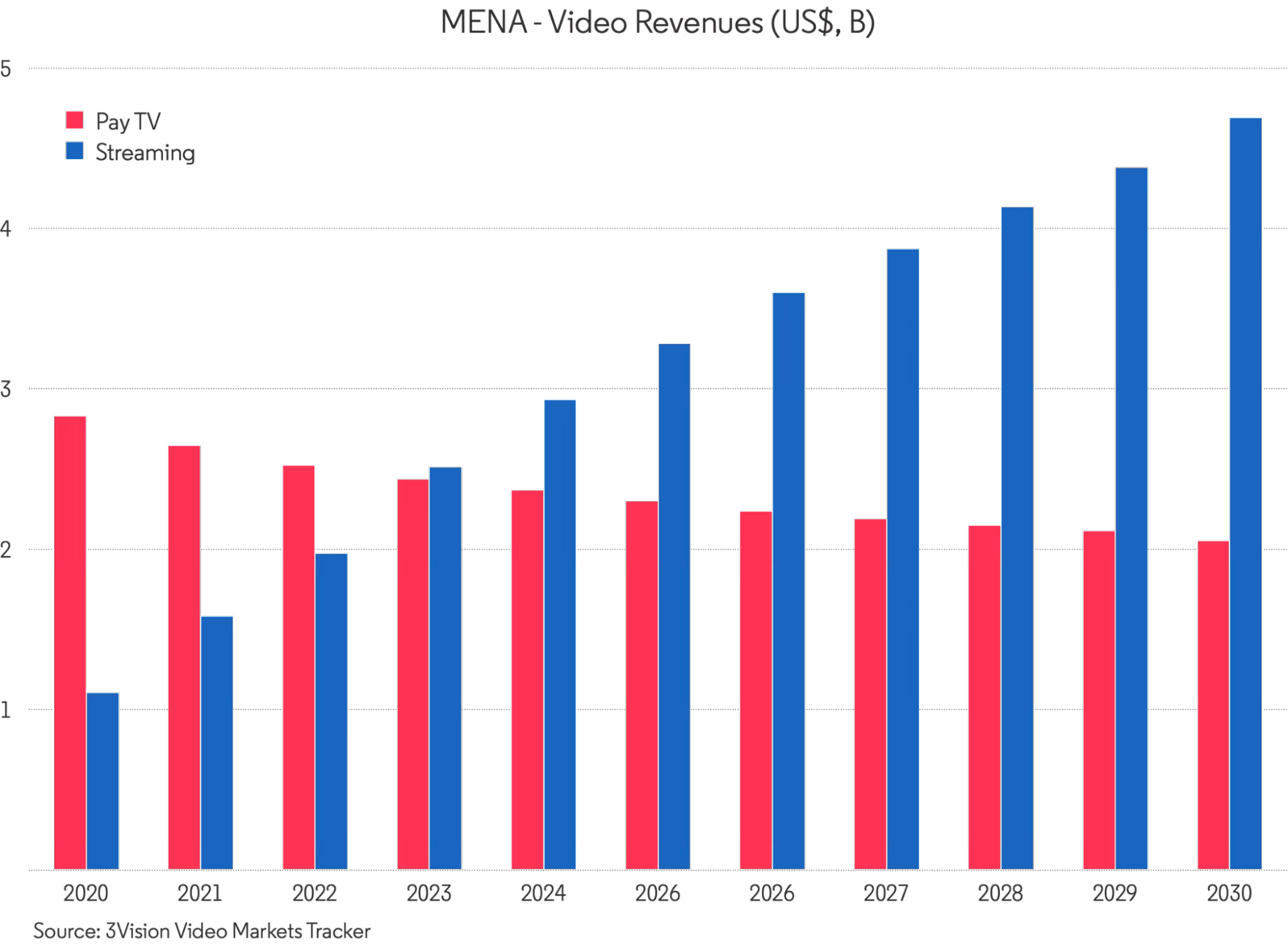

3Vision's latest Video Markets Tracker forecast confirms that while free-to-air linear TV remains dominant across the Middle East and North Africa, streaming has become the primary engine of OTT revenue growth in the region — with SVOD subscriptions on track to reach 50 million by 2030. Total Streaming revenues will rise from approximately $4.6bn in 2025 to nearly $7bn by 2030, widening the gap with traditional Pay TV and pulling decisively ahead by the end of the forecast. Over the same period, SVOD revenues increase from around $3.2bn to $4.7bn, while total AVOD expands from roughly $1.2bn to $1.9bn. Within this, FAST grows from approximately $189m in 2025 to around $590m by 2030, reinforcing its transition from emerging segment to strategic revenue stream.

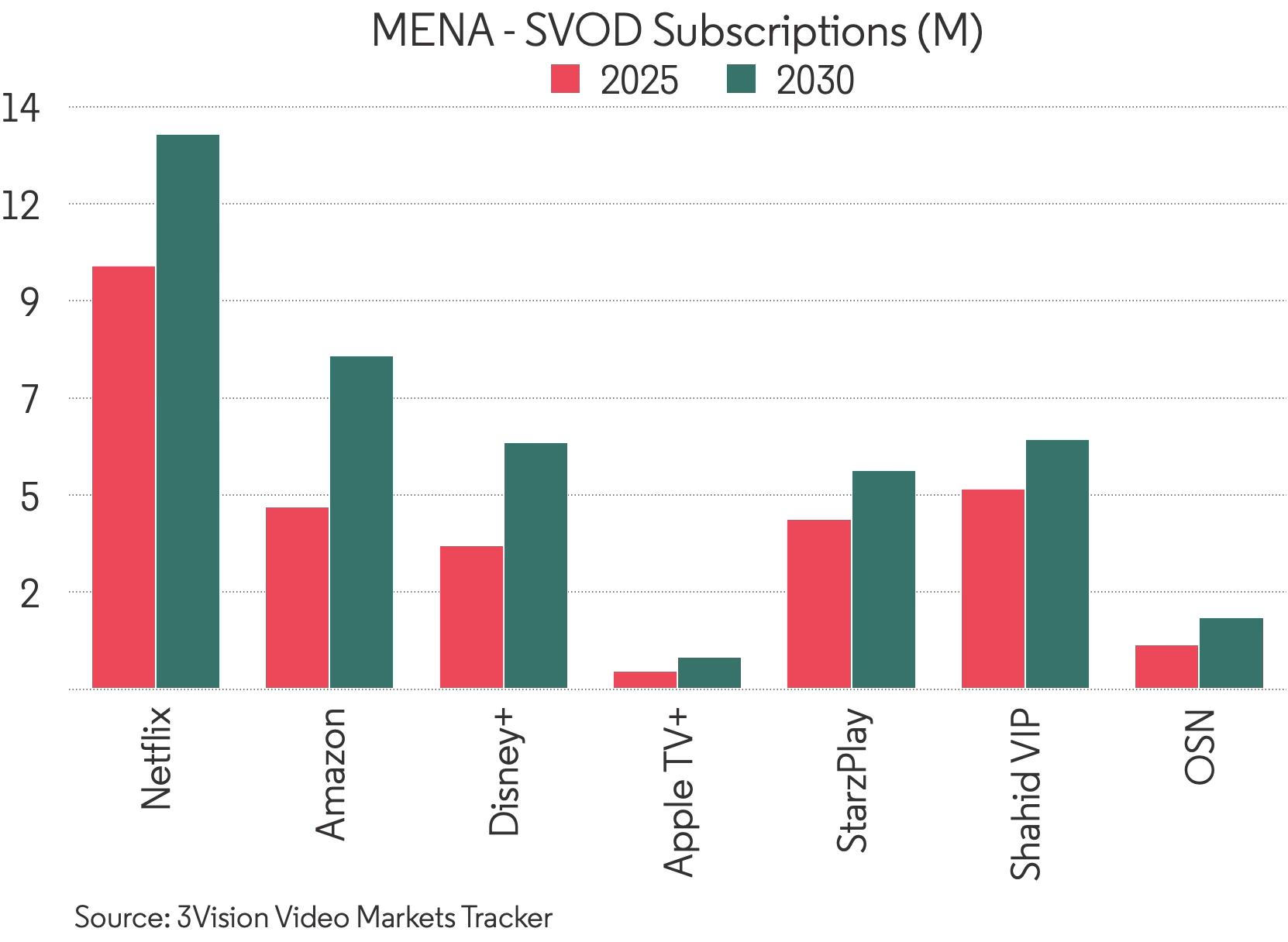

Subscriber momentum tells the same story. According to 3Vision's Video Markets Tracker, SVOD subscriptions climb from roughly 35 million in 2025 to almost 50 million by 2030, meaning around 50% of TV households in the region will pay for at least one service by the end of the decade. By contrast, pay TV subscribers edge up only marginally from around 17.2m in 2025 to 17.8m by 2030, while penetration slips and ARPUs remain under sustained pressure.

MENA SVOD Platforms: Shahid VIP, Netflix, StarzPlay and OSN+ in 2025

The hierarchy of MENA Streaming platforms has evolved considerably. Regional players such as Shahid VIP, StarzPlay and OSN+ used to compete closely with global entrants on scale, supported by strong Arabic content pipelines and distribution partnerships.

Middle East OTT Consolidation: Shahid VIP, OSN+ and Disney+ Bundling Strategy

However, recent strategic moves underline a structural shift toward aggregation. The launch of a pan-national bundle bringing together Shahid VIP, OSN+ and Disney+ signals a new phase in regional streaming, where consolidation is used to reduce churn, simplify billing and increase perceived value.

MENA Streaming Market Outlook to 2030: Netflix, Disney+ and Shahid VIP

By 2030, Netflix will remain the clear revenue leader across MENA, with Disney+ firmly established as the second global pillar following its mid-decade rollout. Shahid VIP retains its position as the strongest pan-Arab platform, leveraging MBC’s commissioning power, while StarzPlay and OSN+ occupy more premium, niche positions.

Platform Mergers and Ecosystem Expansion in MENA

Similarly, Abu Dhabi Media’s decision to fold its ADtv streaming proposition into StarzPlay – effectively shuttering its standalone app in favour of integration within a larger platform – reflects a growing recognition that scale and infrastructure matter as much as content libraries. OSN’s merger with Anghami, combining video and music into a broader digital entertainment platform, further reinforces the trend of consolidation and ecosystem expansion over isolated growth.

Pay TV and Satellite TV Decline in MENA: beIN, OSN and the Shift to Streaming

On the Pay TV side, there have been no dramatic regional shutdowns, but the direction of travel is clear. Major operators have not merged outright, yet many are deliberately migrating satellite subscribers toward Streaming equivalents (e.g. OSN+, beIN Connect). Linear pay TV remains present, particularly in satellite-heavy markets, but growth is constrained and strategic focus has shifted decisively toward digital.

Conclusion: MENA's Streaming Market Is Pulling Decisively Ahead

- Revenue Growth: Total OTT streaming revenues in MENA rise from $4.6bn in 2025 to nearly $7bn by 2030, overtaking traditional Pay TV as the region's dominant video revenue pool

- SVOD Expansion: MENA SVOD subscriptions climb from 35 million in 2025 to almost 50 million by 2030, reaching 50% of TV households across the Middle East and North Africa

- FAST Momentum: FAST revenues grow from $189m in 2025 to $590m by 2030, transitioning from an emerging segment to a strategic revenue stream in the MENA video market

- Pay TV Trajectory: Pay TV subscribers edge up only marginally from 17.2m to 17.8m by 2030, with ARPUs under sustained pressure as satellite TV migrates toward streaming equivalents

- Platform Consolidation: Bundling and aggregation — through deals combining Shahid VIP, OSN+ and Disney+ — define the next phase of Arabic streaming platform competition

Explore 3Vision's Video Markets Tracker – detailed forecasts and insights on Global Video Market, including Streaming, Pay TV, SVOD, AVOD, and FAST adoption

.svg)