Originally published by C21

Written by Karolina Kaminska

23rd February 2026

LONDON TV SCREENINGS: UK programming exports are on the up, but according to 3Vision’s Jack Davison, this is more about UK sellers diversifying than a sign market conditions are getting any better.

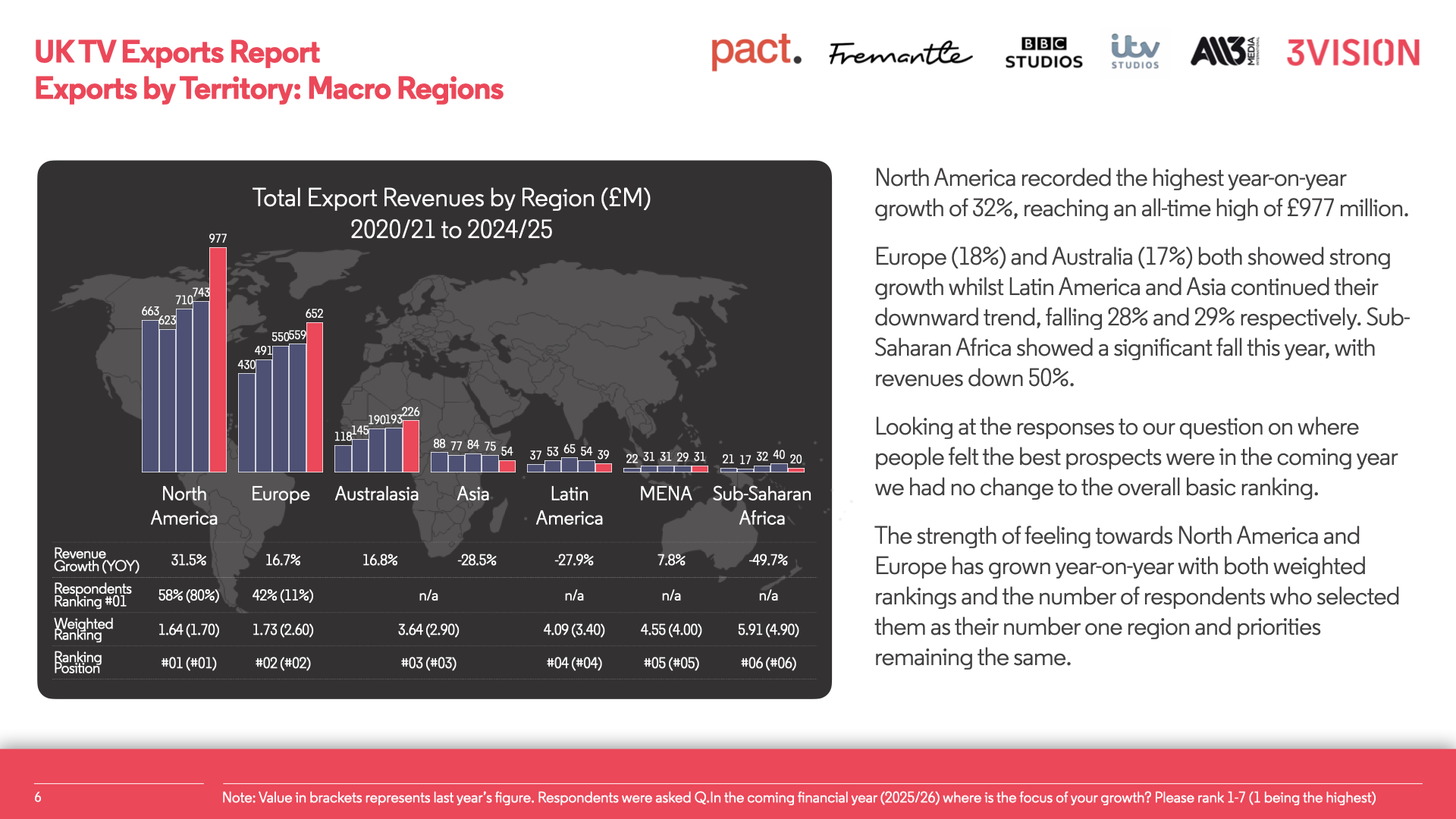

Exports of UK-originated TV programmes returned to growth in 2024/25, increasing almost 11% year-on-year and breaking the £2bn (US$2.6bn) barrier for first time. This came after a near 2% decline in 2023/24 as UK distributors experienced challenging market conditions and a steep decline in coproduction partnerships with the US.

The double-digit growth for 2024/25is certainly good news for the UK industry, as it gathers this week for the London TV Screenings. However, that bounce is more due to the ability of producers and distributors to diversify rather than an end to market challenges, warns Jack Davison, exec VP at 3Vision, which put together the export data for trade body Pact.

“The latest export numbers to some extent defy what has clearly been a tough few years for producers and distributors, but the growth reflects the size, scale and diversity of UK businesses. Conditions are still hard and distributors have had to focus on being diversified, innovative and flexible with everything at their disposal,” Davison says.

This diversification is reflected in the evolution of category shares during 2024/25, with the proportion of overall revenue that was due to TV programming sales declining from 70% in 2019/20 to 53% in 2024/25, despite revenue from TV sales growing in absolute terms.

Within TV programming sales, the share of sales from library content reached a high of 44%, up from 40% in the previous period. This illustrates “both the value established IP is offering video services of all shapes and sizes and how distributors need to work hard in the current climate,” Davison says.

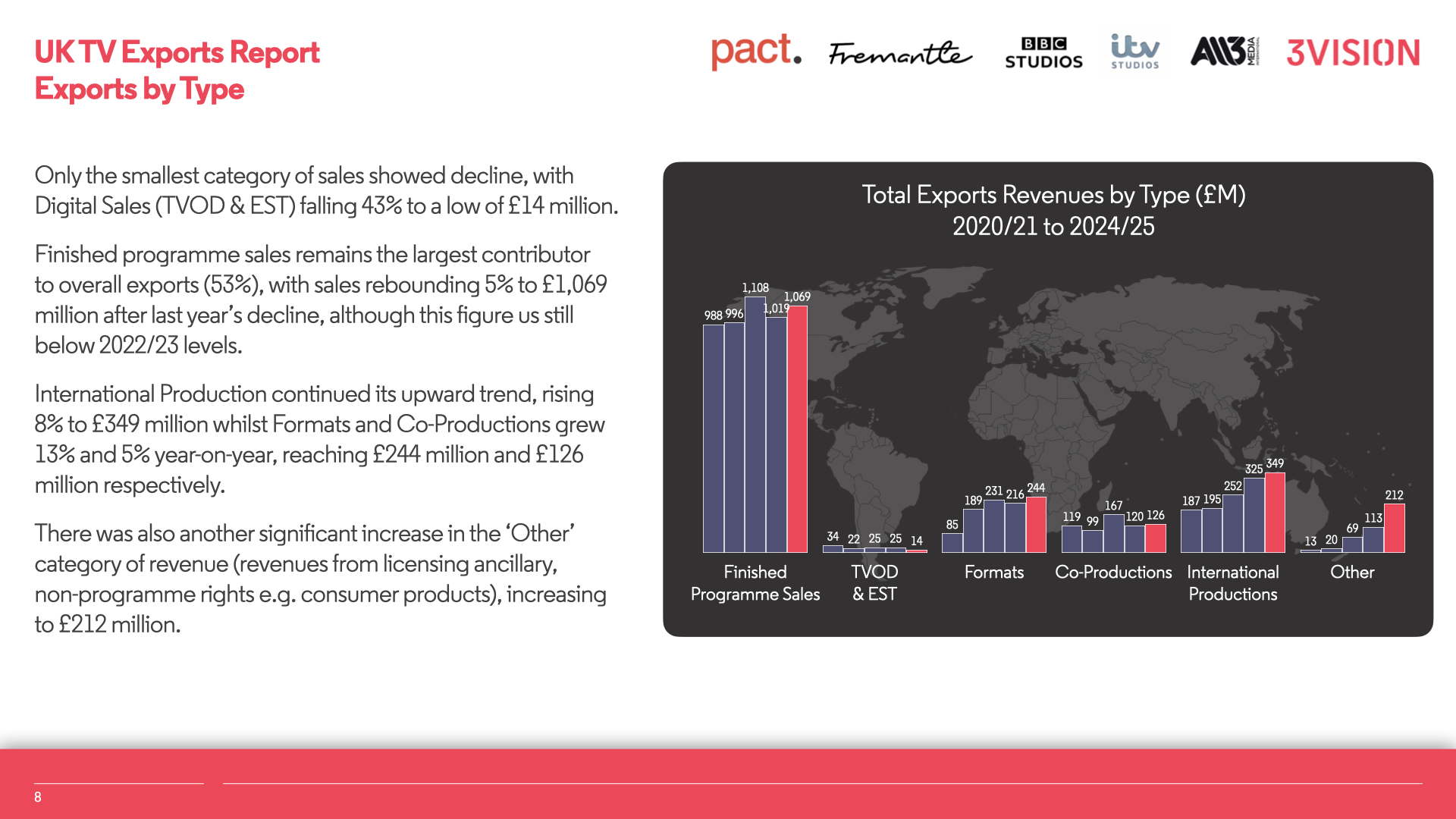

In line with this, finished tape sales grew by 5% year-on-year and remain the largest contributor to overall exports, with 53% of market share.

“There is no doubt that budgets are under pressure; qualitatively, we hear that on a regular basis. Buyers are looking for ways to be efficient; they want to limit risk and get more for their money,” Davison says.

“Streamers from all categories, including broadcaster services, have been having success with older shows and they know what they are getting, and finished tape acquisitions are lower risk and lower budget. With more flexibility around windows and exclusivities, it is all contributing to revised content strategies in global markets.

“The market is shifting as the services themselves experiment and find ways to live with other players. There are more inventive content partnerships emerging, new windowing paradigms and more complexities to deal-making. To optimise revenues, distributors need to work harder to sequence and combine deals because it is through windowing and layering of deals that they can hit the numbers they need to reach. You need a wider and longer view.”

Meanwhile, coproduction revenue rose by 5% year-on-year, after experiencing a 28% drop the year before amid a steep decline in copro partnerships with the US.

According to 3Vision’s ShowTracker in December 2025, there are nine confirmed new-season UK/US copros in the pipeline. Three of these are with HBO and comprise First Day on Earth, Half Man (both coproduced with BBCOne) and War (coproduced with Sky Atlantic). Does this mean the UK/US copro market is back?

“There are signs the market is looking better and feedback is slightly more positive, but in terms of confirmed projects it looks like recovery is at best slow and steady,” Davison says.

“Larger US media companies are still showing caution in total production terms, with only the global streamers upping absolute volumes of new season scripted shows. But HBO has three new-season UK/US shows in the pipeline after having none in 2025, so there are green shoots emerging.”

Furthermore, market consolidation is continuing to ramp up across the industry, with Netflix and Paramount Skydance currently battling it out to buy Warner Bros Discovery; ITV in talks to sell its broadcast business to Sky/Comcast; and RTL buying Sky Deutschland. The more M&A deals that are struck, the smaller the pool of buyers – something that affects not just purveyors of UK content but distributors worldwide.

“We sense some concern among major US studios with European consolidation as they may see consolidation of some of their key buyers. But in some respects that may impact UK players less as these are services more typically active with US content and they often skew more to public service broadcasters,” Davison says.

“In the US, the question will be about what impact this M&A has on production activity, especially coproductions, as any recovery in the market has the potential to be disrupted by M&A.

“There are clearly concerns and all the major markets need to be strategically aware of the different possible outcomes and what that might mean for them – but this could create opportunities as well as challenges.”

All of this comes during a continuation of the economic crisis, which will continue to impact exports of UK programming in the 2025/26 period. Of course, the need for content will still exist, however, requiring distributors to adapt as necessary.

“Uncertainty in global markets is clearly contributing to a market characterised by cautious, risk-averse behaviour. If the current macro climate continues, then producers and distributors will continue to operate in challenging conditions. But services themselves are also facing tough times and the need for great content doesn’t go away – it just adjusts to meet an altered set of objectives,” Davis says.

“The flexibility that businesses need cuts across types of partnerships, rights grants, terms, fees and every element of a deal. Finding the right synergies can help all players involved combat against macro pressures.”

At the London TV Screenings this week, Davis has a message for distributors: “With the levels of content on the market, distributors will know they need to get their proposition across clearly and stand out.The focus needs to be on understanding how values can be exchanged – and agreed – when there are many other moving parts to deals. Sequencing, utilisation, exclusivities, the involved parties and other factors are all at play, and ensuring the values are at the right level will be important.”

Ross Lewis, director of international and projects at Pact, which commissioned the export research from 3Vision, adds: “Despite the global economic challenges, and after several unsettling years across global markets, quality British TV content continues to be in demand for international audiences around the world. A significant shift is happening with the structure of our industry, and those who adapt will prosper.”

.svg)