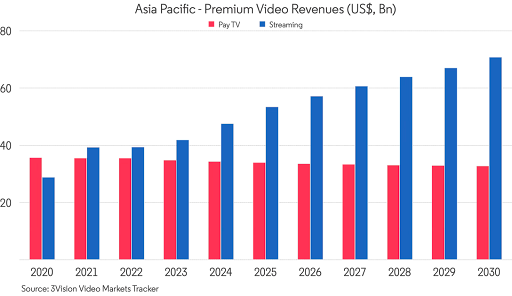

Asia Pacific Video Market Overview: $104 Billion by 2030

Asia Pacific is entering a new era of video growth; one shaped by harsh price sensitivity, mobile-first viewing, and the dominance of ad-supported streaming. According to 3Vision’s Video Markets Tracker, the region's total OTT and video market is set to exceed $104 billion by 2030, with digital video climbing to nearly $71 billion and Pay TV flattening at just under $33 billion.

While these headline numbers signal a continued surge toward streaming, the underlying forces redefining the region are far more nuanced and far more revealing about the future of global video markets.

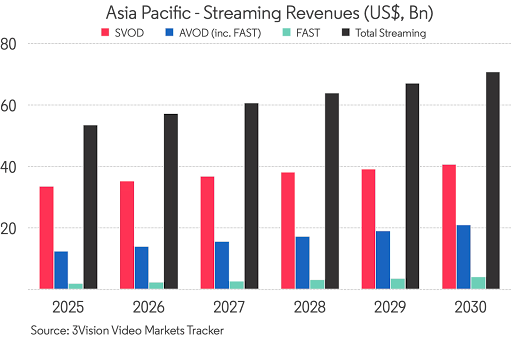

Ad-Supported Video Takes Centre Stage in Asia Pacific's Streaming Market

Advertising-funded video is now the single biggest accelerator of digital revenue in Asia Pacific. AVOD is forecast to grow 69% over the next five years, with FAST revenues more than doubling - together generating over $25 billion by 2030.

This reflects the structural realities of the region: many consumers either cannot afford unsubsidised premium content, while many markets are overcrowded with SVOD services, creating further downward pricing pressure. Ad-supported video on demand revenues are, therefore, set to grow from 23% to 30% over the next five years, as a proportion of total streaming revenue.

FAST, still in early rollout across the region, is benefiting from the rapid expansion of connected TV (CTV) hardware, OEM partnerships, and broadcaster participation – echoing the pattern once seen in Europe and North America, but with deeper telco integration.

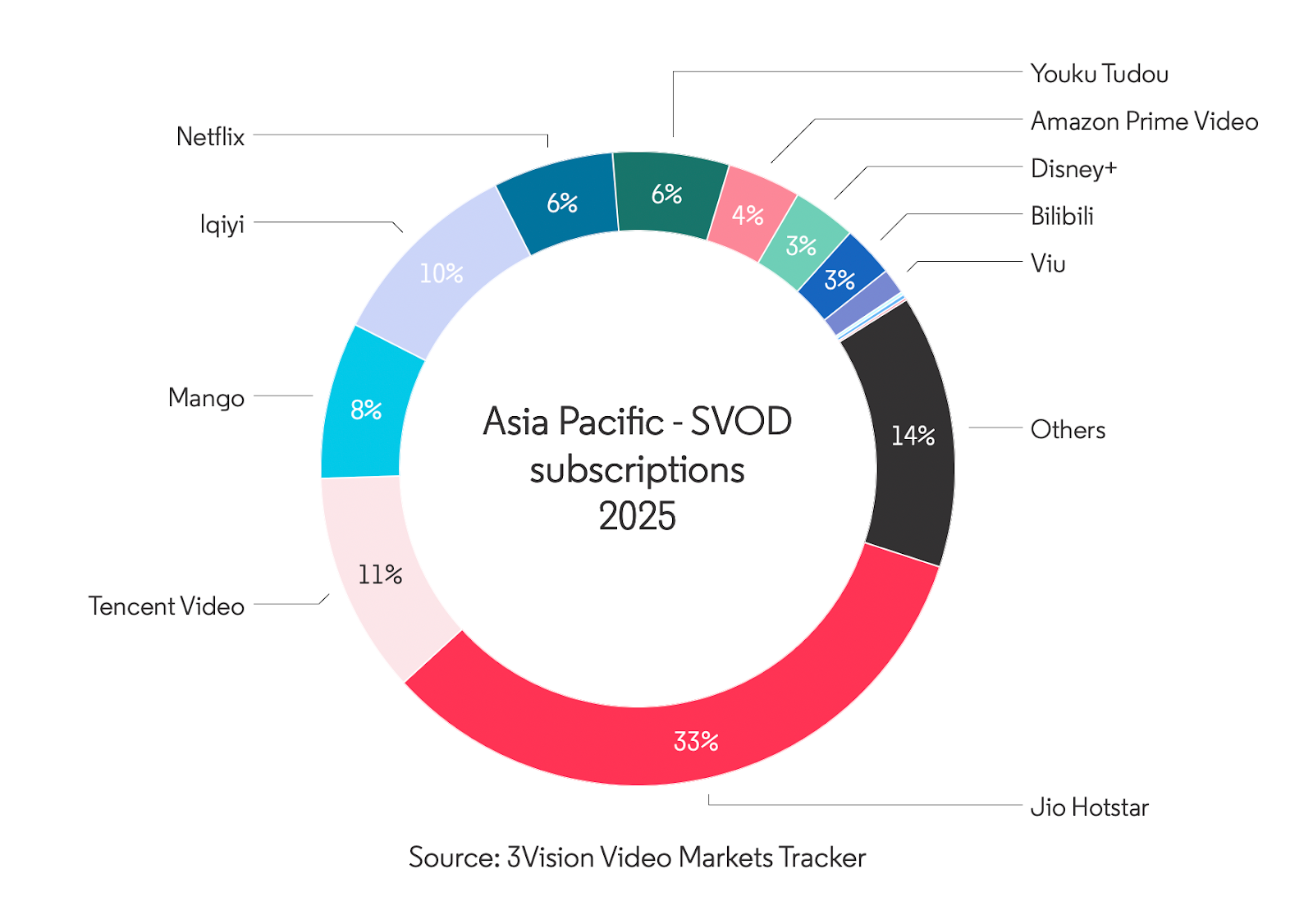

Asia Pacific SVOD Landscape: Growth, But Not Uniform

SVOD subscriptions surpassed Pay TV households last year, establishing Streaming as Asia Pacific’s dominant premium video model. By 2030, SVOD subscriptions are set to hit 1.2 billion, compared to 963 million Pay TV households.

A crucial contextual reality remains: global platforms account for only a minority of subscriptions. Domestic services such as iQIYI, Tencent Video, Youku, Viu and Jio Hotstar continue to dominate the region. Of course, the great Chinese firewall partially preserves this dynamic, but even when looking outside of China, local platforms are more deeply embedded in telco bundles, mobile billing, and content consumption habits.

India's Streaming Market: Jio Hotstar and the Power of Local Sports Rights

This was proven in India, where Jio Hotstar’s explosive customer acquisition following its acquisition of IPL cricket rights demonstrates two key truths. For one, local content - especially sports - remains the single most powerful driver of scale in the region. Secondly, this success was not achieved by a Western streamer in isolation. Instead, the platform that benefited most was a domestic hybrid operator that ultimately absorbed Disney’s Hotstar business. While we are sceptical that the reported 300mn+ subscribers to Jio Hotstar are sticking around for an entire year (rather than just hopping onto a plan during IPL season), its seismic impact on the market cannot be understated.

Why Telcos Hold the Keys to APAC Streaming Market Growth

Asia Pacific’s growth is not just a story of content and platforms; it is a story of infrastructure. Across the region, mobile operators are the true power brokers of Streaming distribution. Their influence stems from massive smartphone penetration, offering them direct access to billions of connected devices and pre-existing customers. This allows operators to bundle Streaming services into prepaid and postpaid plans with frictionless billing.

To a lesser extent, this also applies with first screens. Telcos in Asia Pacific are finding their feet as FAST and AVOD distribution channels via CTV and super-app ecosystems, although this is a well-trodden path in some leading markets (think Japan, South Korea etc.)

With operators gatekeeping many digital audiences, successful streaming plays in the region increasingly resemble partnership ecosystems rather than standalone services.

Asia Pacific Video Market Outlook to 2030

By 2030, APAC’s video economy will see ad-funded models becoming central to digital scale, while telco bundles will remain the backbone of subscription growth. Local content and rights will continue to dictate platform performance as global Streaming platforms focus on value per subscriber, not raw scale. Furthermore, hybrid tiers will become the norm in premium markets.

In short, the Asia Pacific streaming market is not just a fast-growing region – it is the blueprint for the global streaming evolution. A market driven by mobile distribution, hybrid monetisation, and culturally rooted content will set the tone for how streaming platforms worldwide rethink scale, revenue, and competitive strategy.

Conclusion: Asia Pacific Is the Blueprint for Global Streaming

- Market Scale: Asia Pacific's total video market exceeds $104bn by 2030, with digital video reaching nearly $71bn

- Ad-Supported Dominance: AVOD grows 69% over five years, with FAST revenues more than doubling — together generating over $25bn by 2030

- SVOD Growth: SVOD subscriptions hit 1.2 billion by 2030, surpassing 963 million Pay TV households

- Local Platforms Lead: Domestic services including iQIYI, Tencent Video, Youku, Viu and Jio Hotstar dominate over global platforms across the Asia Pacific streaming market

- Telco Distribution: Mobile operators remain the backbone of APAC streaming market growth, bundling services into prepaid and postpaid plans at scale

- Hybrid Models: Hybrid ad-supported tiers become the norm in premium markets as global streaming platforms prioritise value per subscriber over raw scale

Explore the Video Markets Tracker – detailed forecasts and insights on Global Video Market, including Streaming, Pay TV, SVOD, AVOD, and FAST adoption

.svg)