One of FAST’s core value propositions is that it offers viewers a more relaxed viewing experience by eliminating the decision fatigue typically associated with on-demand streaming platforms. Initially, the move towards linear programming was intended to provide a more concentrated and curated content selection. However, several major FAST platforms are still expanding their lineups at a pace, which is potentially diminishing the intended lean-back experience. Nevertheless, the question remains: what is the ideal number of channels for a FAST platform?

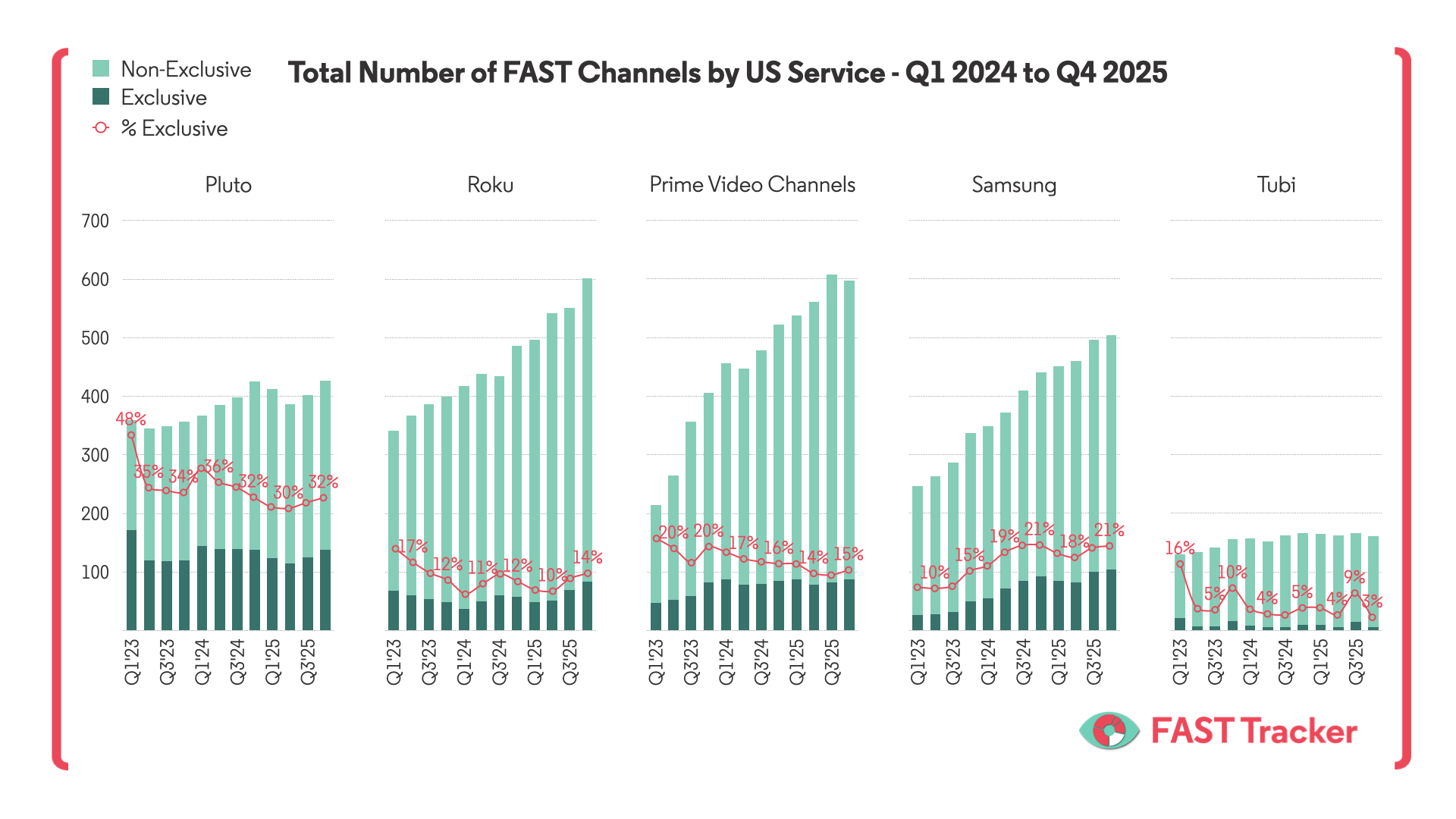

In the United States, most of the major streaming platforms have over 400 channels, and continuously increasing. Notably, several prominent services, including Roku, Prime Video, and Samsung TV Plus, are still expanding their channel lineups at a remarkably rapid pace. However, Tubi stands out as an exception, with a relatively small channel lineup of just over 150 channels (excluding local news retransmissions) and minimal growth in the past two years. Pluto, similarly, adopts a more considered approach, likely influenced by their resource-intensive O&O-centric strategy, which maintains a higher percentage of exclusive channels but reduces the overall number of channels.

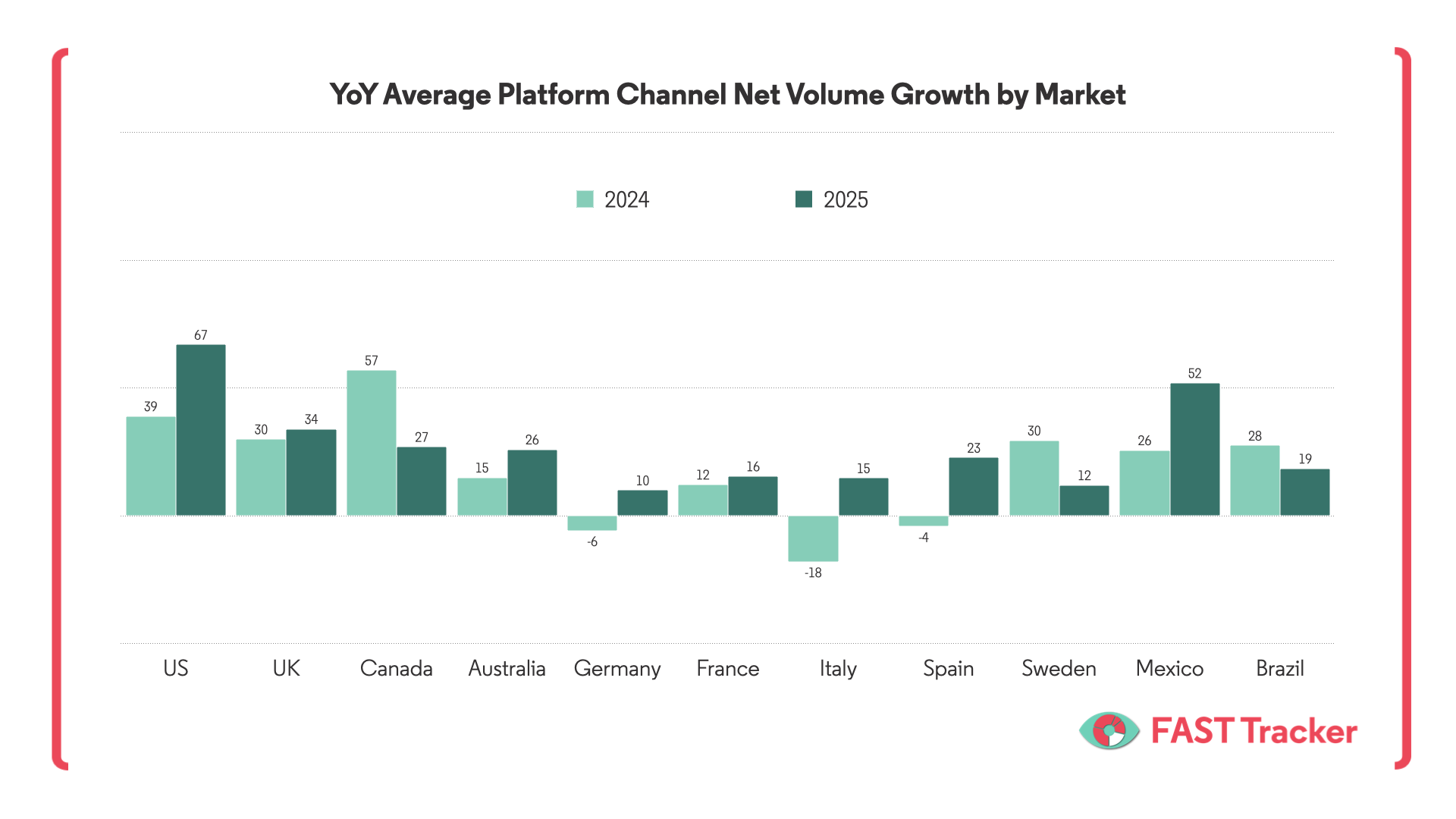

Similarly in Europe, after showing signs of hitting a channel volume ceiling in 2024, last year brought new growth back to the platforms, driven by the continued involvement of local Broadcasters and other Tier 1 channel brands. Generally, platforms in the UK are pushing over 200 channels, while those on the continent mostly have over 150 in each country, each showing a significant preference for localised or local content.

With the increasing number of channels available on EPGs, the competition for viewers’ attention intensifies and with that the competition for ad dollars. In the ad-supported industry, where steady viewership is crucial for generating reliable revenue, when does a channel become economically unviable?

While FAST channels typically cost a fraction of a traditional broadcast channel, profit still needs to be at the forefront of the conversation. Many of the metrics in the FAST world have been growing, but with the increasing volume of channels in the market it is becoming more challenging to fight for share of advertising revenue and channels will need to reach profitability - in much the same way as the SVOD streamers faced up to reality in 2022 and switched their lens from subscriber growth at all costs to streaming profitability. FAST channel operators have many considerations as they seek profitability. The proposition needs to be right but then there are also many other less controllable factors such as discoverability and advertising monetisation that directly influence revenues.

So while there FAST market continues transition to higher quality content (and increase costs), it will be interesting to see how the channel owners chase profitability.

.svg)