In 2025, Disney’s scripted series are heading for new homes.

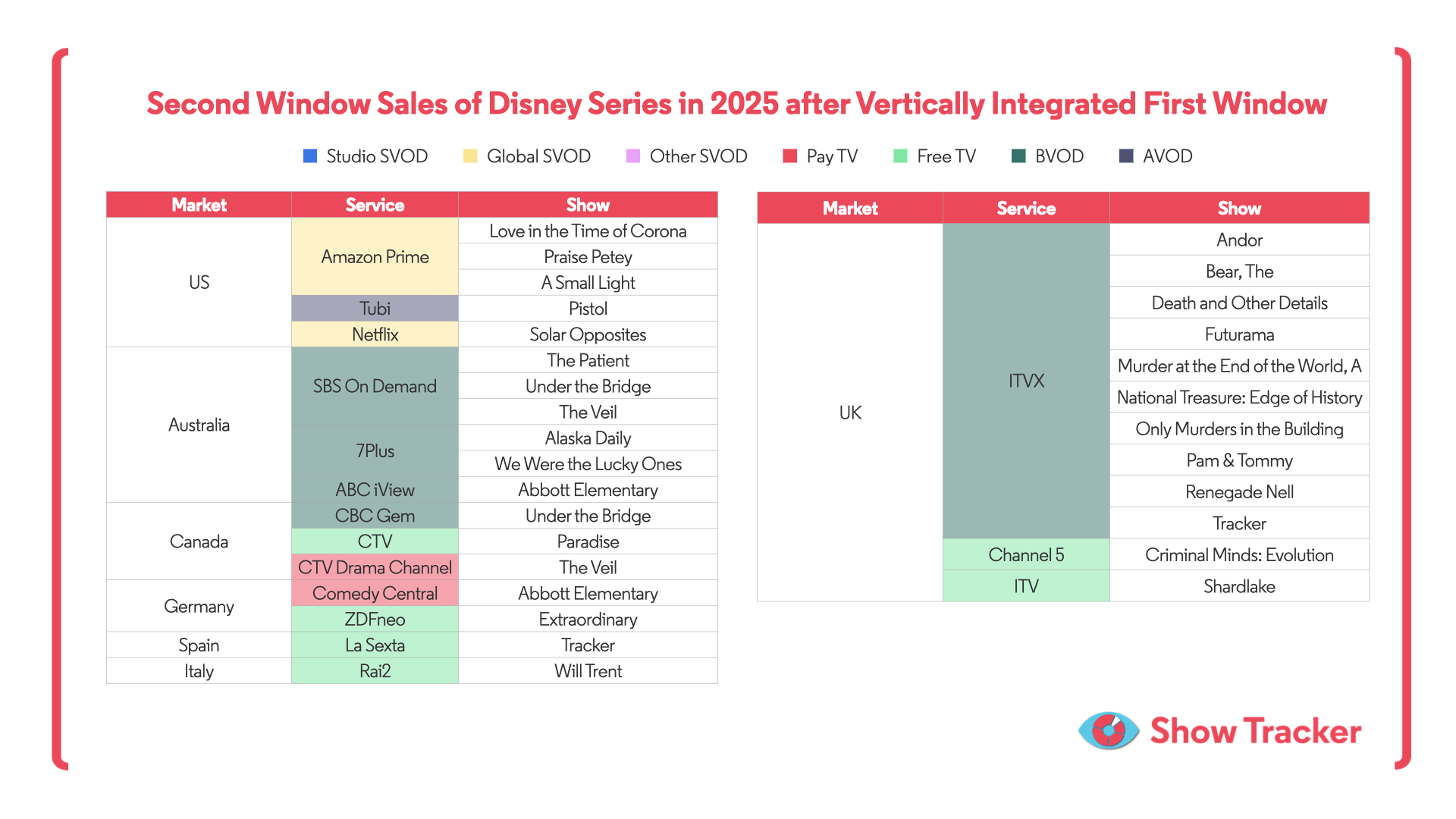

Following initial runs on Disney+ and Hulu, a wave of titles has entered second-window distribution across key global markets. In the US, Amazon Prime has emerged as the primary buyer. Elsewhere, Free TV and BVOD services are proving the most active, with buyers in Australia, Canada and the UK acquiring a broad range of Disney content.

This post-streaming activity offers a revealing snapshot of how rights strategies are evolving - and which players are gaining ground.

Amazon Prime Video is the dominant second-window buyer for Disney series in the US. Titles such as 'Love in the Time of Corona', 'Praise Petey', and 'A Small Light' have been acquired for the platform. Netflix has also more recently picked up ‘Solar Opposites’, adding to its adult animation slate with acquisitions.

Notably, 'Pistol' has landed on AVOD service Tubi - and is the only title in this group to be removed from Disney+ entirely, following an impairment write-off.

In Australia, second-window sales have favoured local BVOD platforms. SBS On Demand, 7Plus, and ABC iView have picked up titles including 'The Veil', 'Under the Bridge', and 'Abbott Elementary'.

A similar picture emerges in Canada. CTV and CBC Gem have acquired several high-profile shows, reflecting a clear appetite among ad-supported platforms for premium US content.

In both cases, BVOD is outpacing Pay TV and SVOD for these rights - a shift that reinforces its growing strategic importance in the content lifecycle.

In the UK ITVX began a partnership with Disney to include a new “A Taste of Disney+” branded rail on ITVX, offering select series to ITV audiences while directing viewers to full boxsets on Disney+. The relationship between the two pre-date this, with ITVX acquiring many second windows previously such as ‘Renegade Nell’, ‘Under the Banner of Heaven’ and ‘Welcome to Chippendales’.

For Disney, these sales mark a notable shift. While content continues to debut on Disney+ or Hulu, a more open approach to second-window licensing is now in play.

It’s a strategy that, as opposed to Paramount, is more open to local buyers generally - particularly those in Free TV and BVOD - and reflects a broader move away from exclusivity being made available for the second window.

.svg)